Understanding Mexico's economic landscape via data transformations

Stay informed with the latest insights on Mexico's economy via statistics and AI analysis and synthesis.

Stay informed with the latest insights on Mexico's economy via statistics and AI analysis and synthesis.

El Economista Argentinian President Javier Milei intervened in the foreign exchange market just days before crucial legislative elections, as the peso plummeted to 1,400 per dollar before recovering to 1,365 following Treasury announcements. The official dollar reached its highest level since the removal of currency controls in April, with the government selling dollars to stabilize the market amid rising country risk and volatility. Analysts expressed concerns over the government's lack of reserve accumulation and the dismantling of liquidity instruments. While the peso showed slight recovery, Argentine sovereign bonds fell over 3%. The S&P Merval index gained 1.85% after a previous decline. The intervention aims to manage exchange rate volatility, particularly in the tense electoral climate. Milei interviene en el mercado de cambios a días de las elecciones

El Economista The Bank of Mexico (Banxico) acknowledged that domestic investors are orderly absorbing Mexican debt, compensating for a $25.7 billion liquidation by foreign investors over the past 15 months. As of September 2025, foreign ownership of Mexican debt stands at 12%, down from 14% in April 2024 and 28% in December 2019. The report highlights that local institutional investors, particularly Siefores, hold 28.8% of the total debt, up from 24.6% in December 2020. Despite global uncertainties, Mexico remains attractive due to its fiscal discipline. The IIF noted that high real interest rates and a stable exchange rate are generating solid returns, with expectations of continued inflows despite potential global demand declines. No specific forward guidance or upcoming decision dates were mentioned. Mercado doméstico compensa liquidación de deuda mexicana

El Economista The Eurozone's inflation rose slightly to 2.1% in August 2025, up from 2.0% in July, according to Eurostat. This increase is attributed to a slower decline in energy prices, which fell by 1.9% compared to a 2.5% drop in July. Core inflation, excluding volatile items, remained stable at 2.3%. Analysts had expected inflation to hold at 2.0%, aligning with the European Central Bank's (ECB) target. The ECB is anticipated to maintain interest rates at its upcoming policy meeting on September 11, following a pause in rate cuts since July. Key risks include fluctuating energy prices and food inflation, which decreased to 3.2% from 3.3%. Inflación en zona euro aumentó ligeramente durante agosto

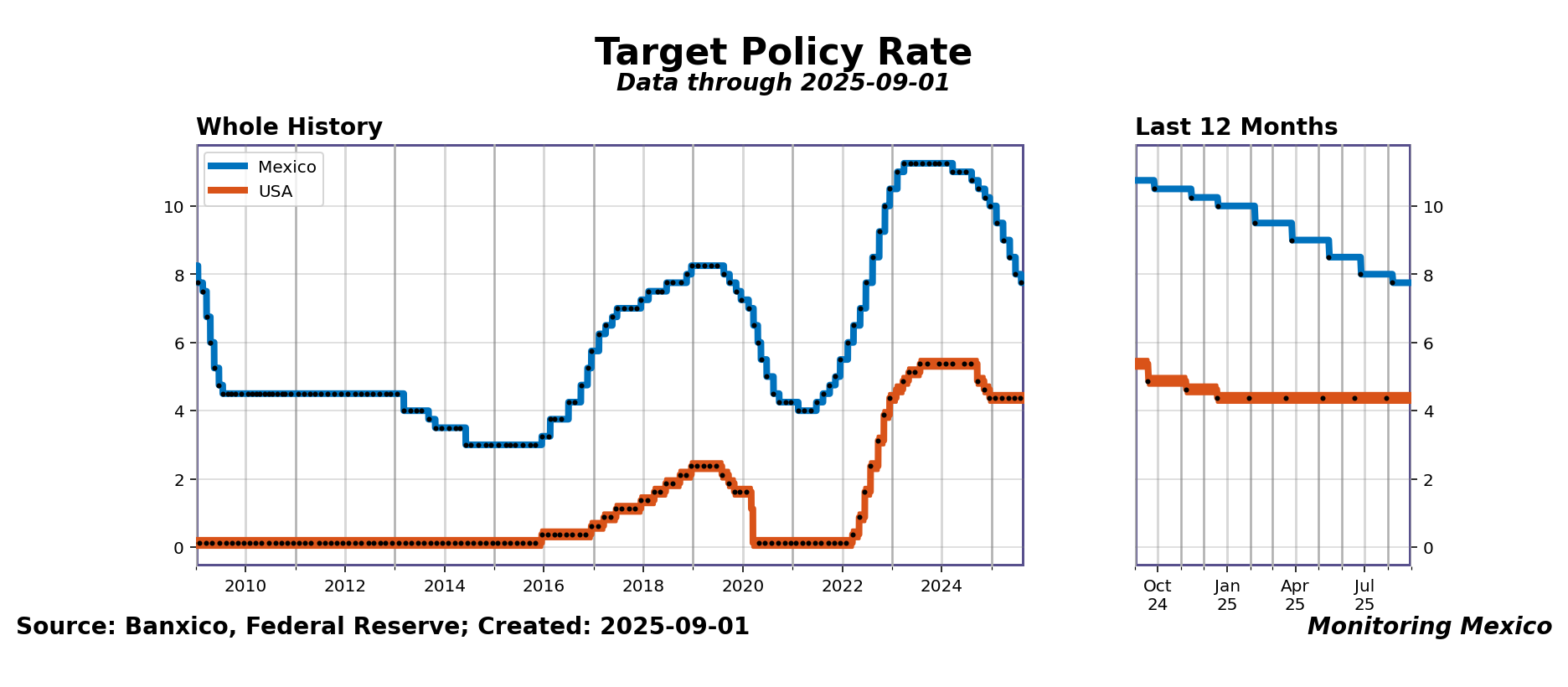

Banxico’s policy rate sits at 7.75%, maintaining a long easing streak. Mexico’s policy rate stands at 7.75% as of September 1, 2025, following a 0.25 percentage point cut in early August. This marks the ninth consecutive reduction since August 2024, amounting to a cumulative 3.25 percentage point easing over roughly 13 months. There has been no policy reversal since March 2023, signaling a sustained accommodative stance. Domestic financing conditions remain closely watched amid growing concerns around Mexico's structural economic challenges. With three policy meetings left this year, the central bank appears poised to sustain its current approach while monitoring these longer-term headwinds.

The Fed’s slower adjustments contrast with Banxico’s more aggressive easing. In the U.S., the federal funds rate averages 4.38% as of September 1, 2025, following a 0.25 percentage point cut in December 2024. The Fed’s moves toward easing have been more gradual, with the last rate hike dating back to July 2023, similar to Banxico’s timeline for its last increase. Historically, the Fed has often acted first, with Banxico following, frequently in a one-move-one-hold pattern this year. This timing dynamic underscores the careful calibration both central banks exercise amid their differing economic landscapes.

Divergent monetary paths elevate risks around capital flows and inflation control. The ongoing policy divergence raises questions about capital movement volatility and potential peso depreciation pressures. Mexico’s higher rates grant it some insulation, yet the shadow of elevated structural economic uncertainties complicates the outlook. Maintaining policy autonomy will require balancing inflation risks, which could be reignited through pass-through effects especially if external forces shift unexpectedly. Market expectations remain sensitive to these shifts, with policymakers walking a tightrope between sustaining growth and ensuring financial stability under persistent structural strains.

Why the policy rate matters: it sets the cost of money for the whole economy. When the rate is high, borrowing is costly but saving becomes attractive; when low, credit is cheaper and growth gets a boost. Over time, these choices shape investment, jobs, and inflation. Exchange rates also react: if Mexico’s rate is higher than in the U.S., the peso tends to strengthen as investors seek better returns; if lower, the peso can weaken. This link explains why markets watch both Banxico and the Fed so closely.

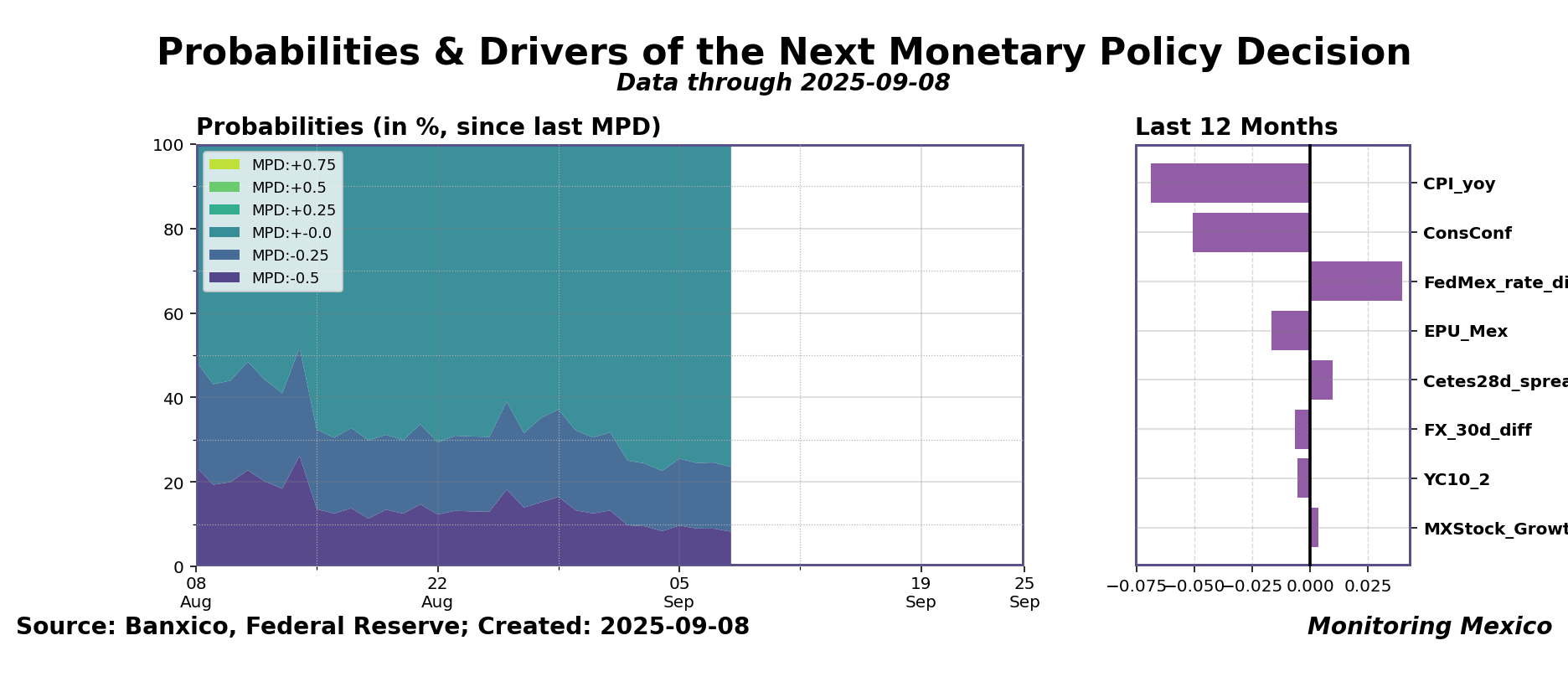

Probabilistic data signal a near 8 basis-point rate cut on 25 September 2025. The mean expected policy move for 25 September stands at -0.079%, reflecting a continued easing trend since the last meeting on 07 August which saw a 0.25% rate reduction to 7.75%. The model assigns a 76% probability to no change from the current level and a 15% probability for an additional -0.25% cut. Other potential outcomes carry negligible odds. This marks a material shift towards dovish monetary policy, consistent with ongoing soft inflation readings and moderated consumer sentiment.

Monetary policy drivers weigh domestic disinflation against external risks. The strongest positive driver is subtarget headline inflation, pulling the average expected move further into negative territory. Consumer confidence is weak, supporting an easing bias. The most significant negative pressures arise from lingering uncertainty in Mexican policy environments and the relative interest rate differential with the US Federal Reserve, both restraining the scope for aggressive cuts. Other variables like equity momentum and yield curve slope have limited influence, while policy uncertainty remains moderate and slightly reduces the room for policy loosening. This mix signals a cautious easing calibrated to balance internal disinflation with external vulnerabilities.

Predictability and transparency build trust in monetary policy decisions. When markets and the public can anticipate how and why the central bank acts, uncertainty falls and policy becomes more effective. Clear communication helps businesses plan investments, households make borrowing decisions, and international investors gauge currency risks. Economists often stress the importance of clarity and traceability — the ability to follow and understand decisions step by step. Without it, rate moves risk being misread, causing volatility instead of stability. With it, policy signals are more credible, anchoring expectations and strengthening the central bank’s influence.

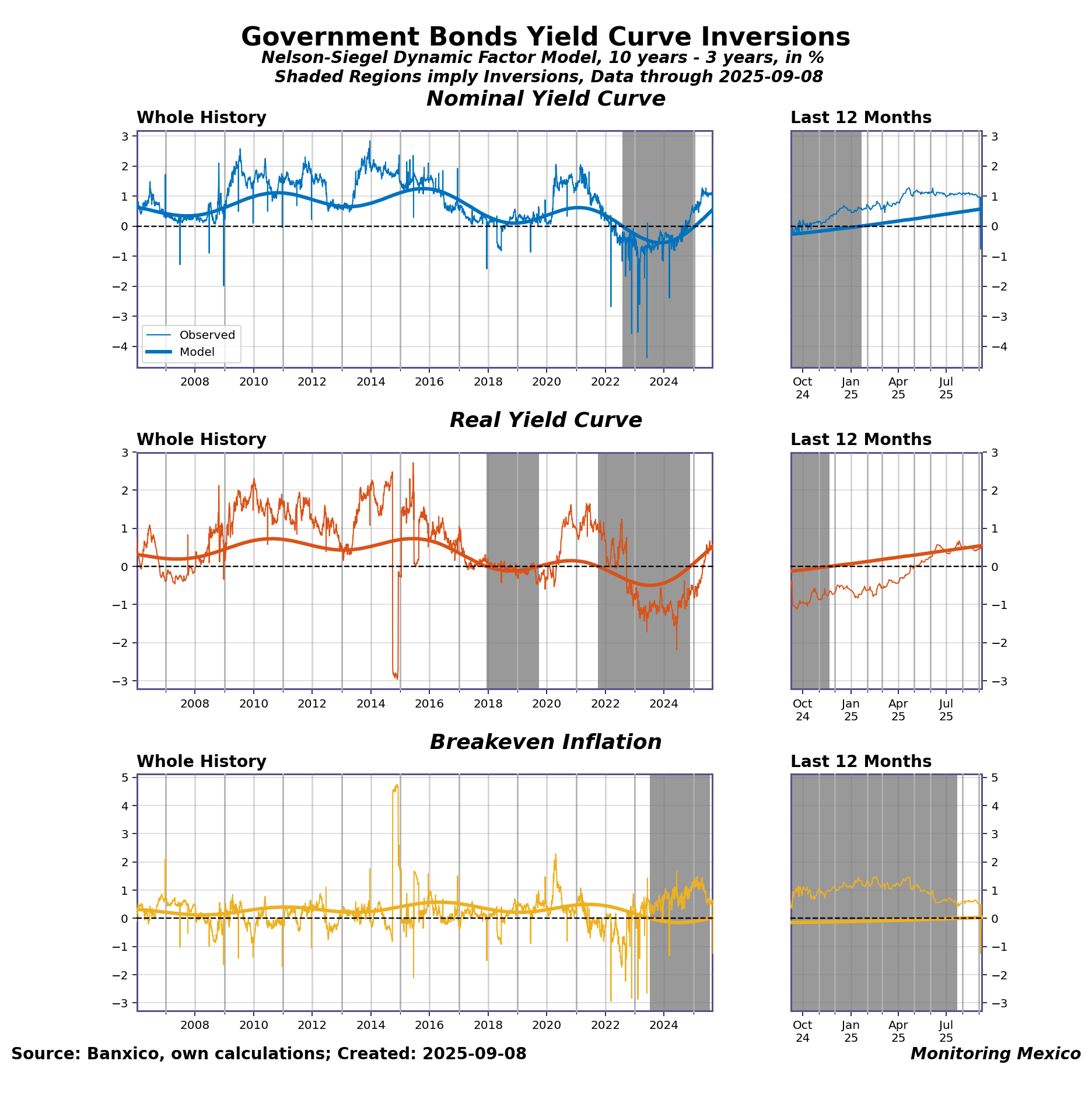

Nominal and real spreads continue to widen alongside subdued inflation expectations. The nominal yield spread between 10- and 3-year government bonds stands at 0.966 daily, above its factor-filtered monthly 0.565, showing a persistent steepening trend over 22 months. Real spreads are near the median daily at 0.477 but elevated monthly at 0.536, marking a 26-month upward trajectory. The implied inflation spread is modest at 0.49 daily and low monthly at 0.029, suggesting anchored inflation expectations despite recent daily volatility. The nominal curve steepening reflects moderate inflation risk premium combined with cautious long-term growth optimism. No curve inversion signals emerging recession fears; overall shapes indicate markets foresee steady inflation and stable policy in the near term.

Market expectations remain critical for policy credibility and financial stability. Investor demand for medium- to long-term Mexican debt is sensitive to shifts in US monetary and fiscal policies, which impose heightened uncertainty on market participants. Expectations about future interest rates and inflation directly calibrate bond yields, influencing borrowing costs and asset valuations across sectors. Clear policy communication aligned with market signals is essential to mitigate volatility and maintain orderly transmission of monetary policy, especially given enduring concerns over external shocks. Managing these expectations helps uphold confidence amid structural and competitive challenges and domestic demand pressures.

Expectations are central for policy effectiveness, and forward guidance is the key tool to shape them. For policymakers, what matters is not only the overnight rate they set, but how markets and households expect rates to evolve over the longer horizon. Households and businesses plan investments, mortgages, and borrowing costs based on multi-year expectations, not just today’s rate. If expectations are aligned with the central bank’s intentions, policy actions transmit smoothly into borrowing costs, investment, and spending. If expectations diverge, the impact weakens or even backfires, causing instability. Forward guidance — communication about the likely future path of interest rates — is designed to reduce this uncertainty and anchor expectations. It works best when it builds confidence without locking the central bank into rigid promises: if conditions change, overly strict guidance risks credibility. Clear but flexible communication, in contrast, strengthens policy effectiveness by shaping expectations while preserving room to adapt.

So…what is this—and why am I doing it?

This project began with a simple question in 2021: how far can automation take us in the age of computers? Monitoring Monetary Policy in Mexico is an experiment at that frontier. By combining statistical analysis, tailored visualizations, and large language models, it demonstrates how even highly specialized topics—such as Mexican monetary policy—can be made more accessible, relevant, and insightful.

When does data stop being a dump and start being a story?

The initiative builds on my earlier Monitoring Mexico project but has since evolved in important ways. Data is no longer simply displayed; it is analyzed, distilled, forecasted, visualized, interpreted, narrated, and contextualized. In short, raw information is transformed into understanding.

Who’s in charge here—a Raspberry Pi or common sense?

Behind the scenes, the site runs on a Raspberry Pi 5 powered by Python and a library of custom routines. Automation drives much of the process, but human expertise remains essential in designing the explanation and presenting the material. The balance between machine efficiency and human judgment is what makes the project work.

How do we cut through the jargon and keep the signal?

The aim is straightforward: to bring clarity to an area often obscured by technical detail. Monetary policy shapes households, firms, and markets, yet its analysis usually remains confined to experts. By filtering, explaining, and visualizing the data, this project seeks to make that knowledge more transparent and more useful.

Is this the 80/20 rule you learn in business school in the wild?

At its core, the site is both a contribution to public understanding and an exploration of how informational value is created. It is a humble attempt to deliver 80% of the insights of a central bank analysis with 20% of the resources—while also testing what the future of knowledge generation might look like.

What might be new the next time you drop by?

This is very much a work in progress, with new features, analyses, and visualizations added over time. We can now at the brink of generating our very own economic policy uncertainty (EPU) index, and we consider a newsletter. But maybe a chatbot might be more appropriate? Coming back to check for updates is always a good idea. If the site sparks curiosity, fosters dialogue, or simply helps illuminate Mexico’s economic dynamics, it has achieved its goal.

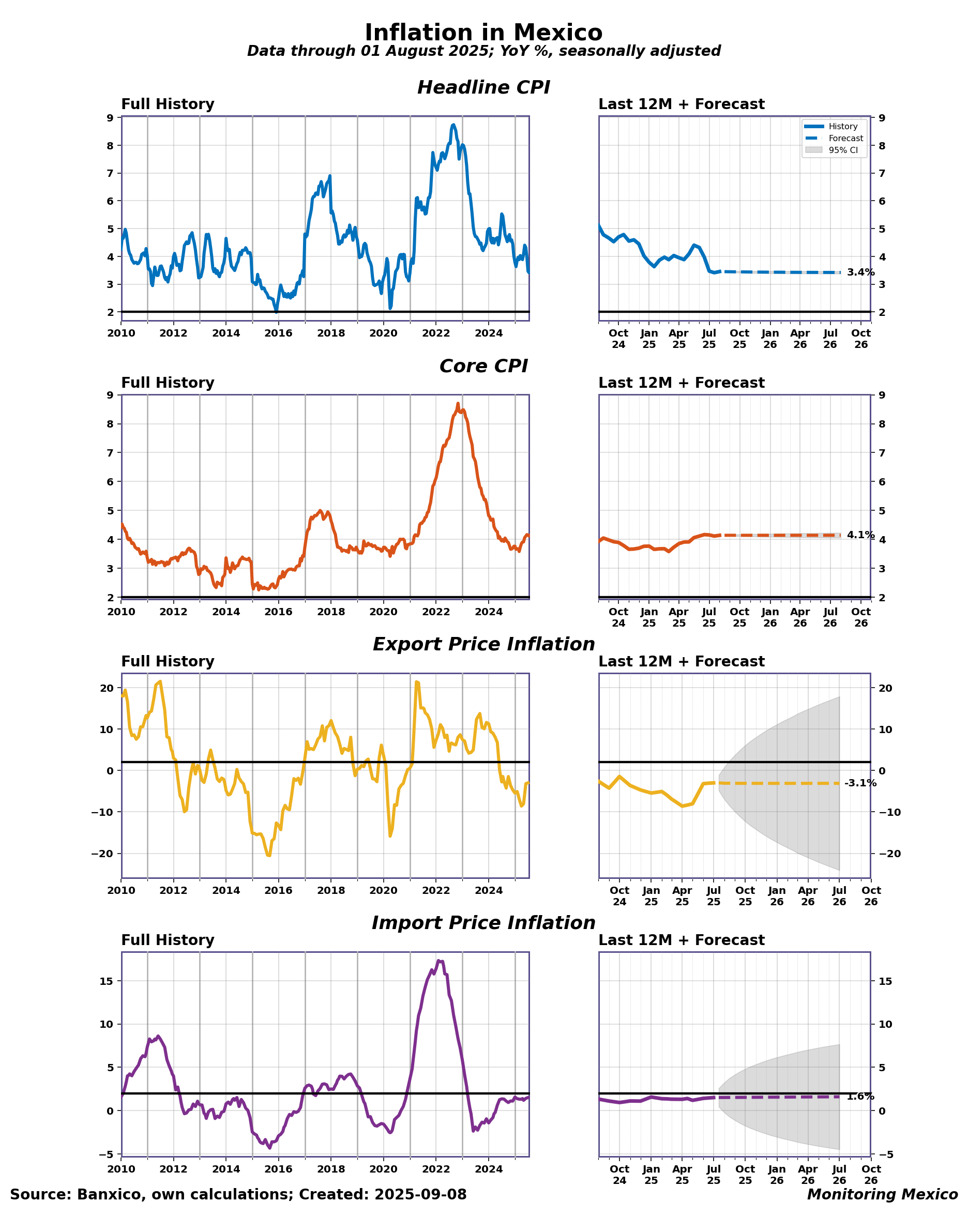

Consumer price inflation remains above target but shows signs of moderation. August 2025 headline inflation was 3.45% year-over-year, above Banxico’s 2% target but down 1.67 percentage points from last year. The recent 0.0396 percentage point monthly increase continues a modest upward trend after two months below this level. Inflation remains historically moderate with no extreme outliers observed in the past year. Longer-term forecasts hold steady at 3.4% for the next 12 months. Growing concerns about external policy shocks and their indirect impact on demand underscore the cautious inflation outlook and implications for monetary policy calibration.

Core inflation remains elevated compared to headline inflation, indicating persistent underlying price pressures. Core inflation registered 4.14%, notably above headline inflation, reflecting more stubborn domestic price dynamics excluding volatile items. Compared to a year ago, core inflation rose 0.212 percentage points and is expected to stabilize around 4.1% over the next year. This indicates an enduring inflation baseline influencing wage and price-setting behaviors.

Import and export price inflation display divergent trends, impacting trade-sensitive price levels. Export prices declined 2.99% year-over-year in July, reflecting ongoing external demand pressures and subdued commodity price trajectories. Conversely, import prices rose 1.51%, indicating cost pressures from abroad that could feed into domestic inflation. Export price inflation improved slightly month-to-month but remains on a multi-month downtrend, while import prices have increased steadily over four months. These divergent inflation paths highlight external vulnerabilities amid heightened concerns over US policy shocks, which contribute to uncertainty in trade and investment conditions. Near-term forecasts point to continued subdued export price inflation around -3.1%, with import prices modestly rising near 1.6% over the coming year.

Price indices are central for monetary policy because they capture both domestic pressures and global shocks. The Consumer Price Index (CPI) is the headline measure of inflation, showing how the cost of living changes for households and whether the central bank’s target is being met. Core CPI strips out volatile food and energy prices, revealing underlying inflation trends that guide sustainable policy choices. Import and export price indices extend the picture by linking Mexico’s inflation outlook to global markets: higher import prices can feed directly into consumer costs, while shifts in export prices affect competitiveness and incomes. Taken together, these measures help policymakers distinguish between temporary shocks and persistent pressures, anchor expectations, and anticipate risks that arise both at home and from abroad.

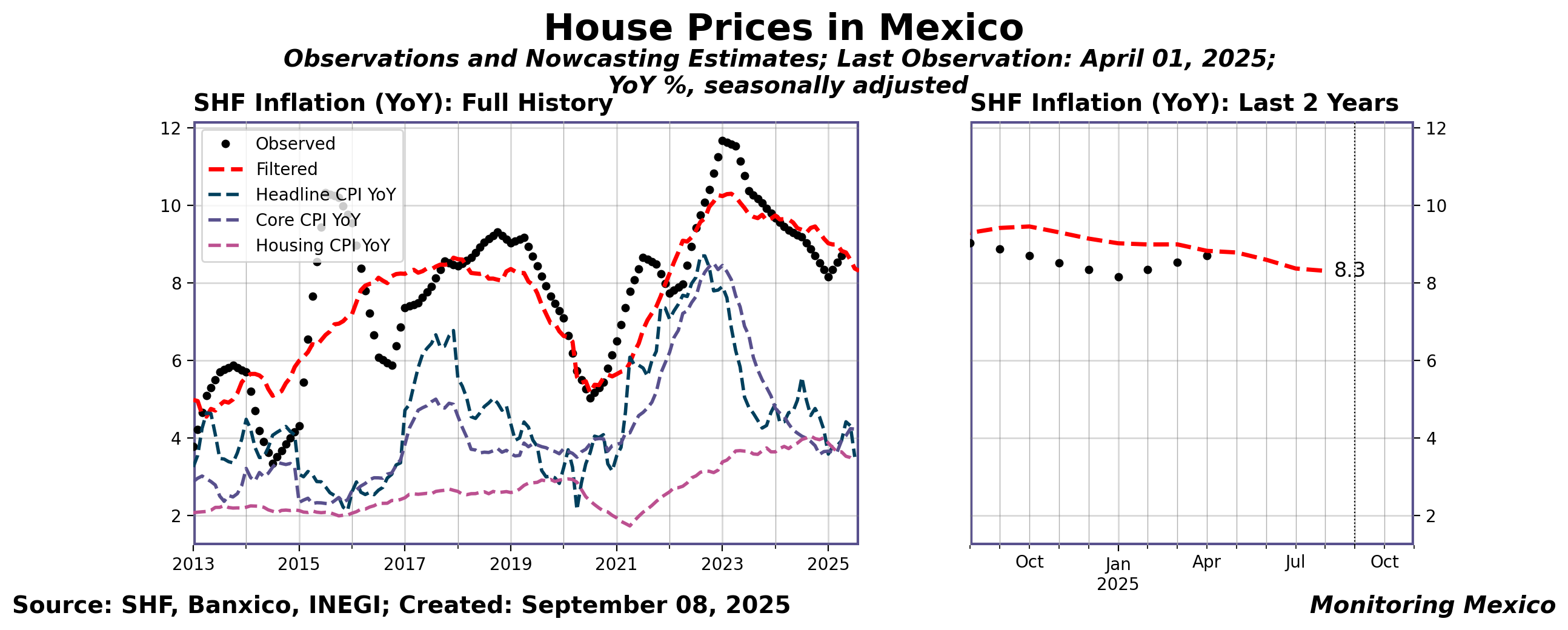

House-price inflation continues to climb, outpacing most consumer price measures amid growing external uncertainties. In April 2025, Mexico's house-price inflation rose to 8.71% year-over-year, near the 78th percentile historically. This marks a third consecutive month of increase, with a 0.187 percentage point rise from March. The pace remains notably above headline CPI inflation at 3.51% and core inflation at 4.23%, as well as the housing cost subcomponent at 3.42%. The ongoing upward trend in house-price growth contrasts with the broader softening in consumer prices, underscoring divergent sectoral dynamics in the current economic environment.

Recent data revisions exert minimal impact but underscore concerns over domestic demand and international policy shifts. Latest news via the dynamic factor model lowered nowcasts for residential construction investment slightly, signaling moderating momentum in related sectors. The biggest single data impact nudged forecasts downward by approximately 0.00 percentage points, reflecting stability rather than volatility in key housing market indicators. Nonetheless, rising apprehension about US policy shocks—remaining at extreme levels—adds a layer of external risk that may influence mortgage markets and capital flows. This backdrop amplifies sensitivity to fluctuations in domestic demand and financing conditions ahead of the upcoming policy meeting.

House prices matter for Mexico’s economy well beyond the real estate market. Housing is often a family’s largest lifetime investment and a key store of wealth. Rising prices can improve household balance sheets and provide collateral for credit, while falling prices can weaken financial security. Housing costs also shape the cost of living, influence decisions to rent or buy, and affect inequality: wealthier households tend to gain from appreciation, while lower-income families face affordability pressures. In Mexico’s context — with a large informal sector and lower mortgage penetration than high-income countries — these dynamics are especially pronounced. Informality limits access to credit, making price increases more exclusionary, and sharp regional differences in housing markets affect mobility and opportunities. Policymakers also monitor house prices for signs of bubbles or instability, since even with modest mortgage depth, volatility in housing markets can pose risks to both financial and social stability.

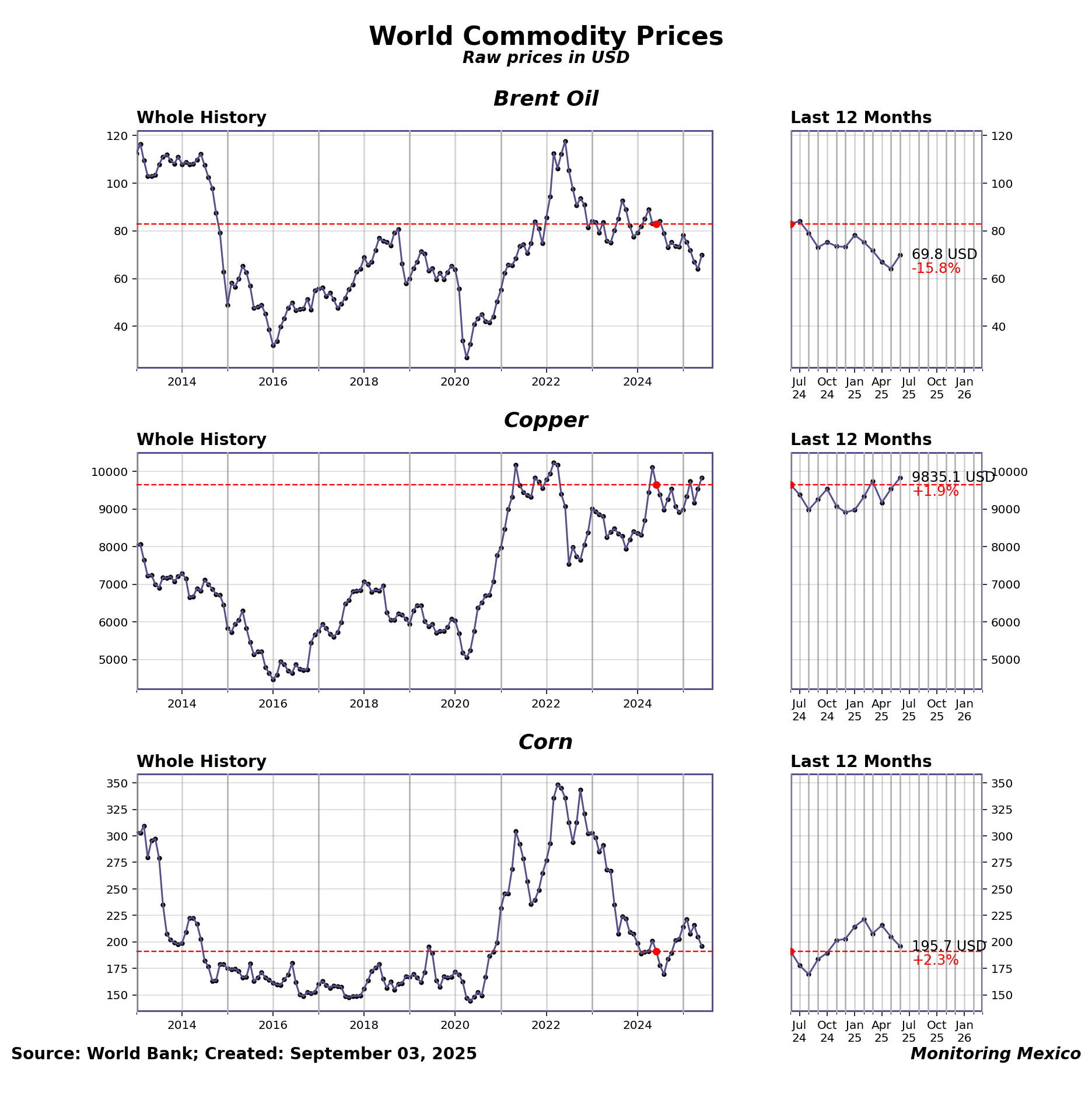

Oil prices are stabilizing but showing signs of modest upward momentum amid broader market uncertainties. Brent oil stood at $69.8 per barrel in June 2025, down 13.1% year-on-year but up 5.75 in the past month. This modest rebound follows a few months of decline, reflecting mixed signals from global demand and supply. Oil remains critical for federal revenue but plays a limited economic role beyond Campeche and Pemex employment, totaling under 1% of national jobs.

Copper prices continue their ascent, supported by strong demand trends and supply constraints. Copper hit $9,840 per ton in June 2025, rising 187 year-on-year and accelerating over recent months. The metal's price momentum underscores its significance, particularly given mining’s 2.4% GDP share, with Sonora accounting for 70–83% of production. Although mining jobs are less than 1% nationally, sectoral shifts here ripples through the economy.

Corn prices are pausing amid slight declines, spotlighting concerns over Mexico’s domestic demand vitality. Corn was priced at $196 per ton in June 2025, up 4.48% year-on-year but falling 9.09 in the last month, marking a two-month downward streak. As a net importer, Mexico’s corn market is sensitive to these shifts despite a MX$290/ton subsidy and some 1.5 million farmers relying on stable prices. Growing unease over domestic demand stresses frames this movement, warranting close attention ahead of policy decisions.

Commodity prices directly affect inflation and signal global economic conditions. Oil and corn feed into energy and food costs, raising living expenses and hitting low-income households hardest. Copper serves more as a signal of global demand, with shifts often foreshadowing business cycle turns. For monetary policy, commodity swings both shape inflation expectations and test credibility, making them critical to monitor.

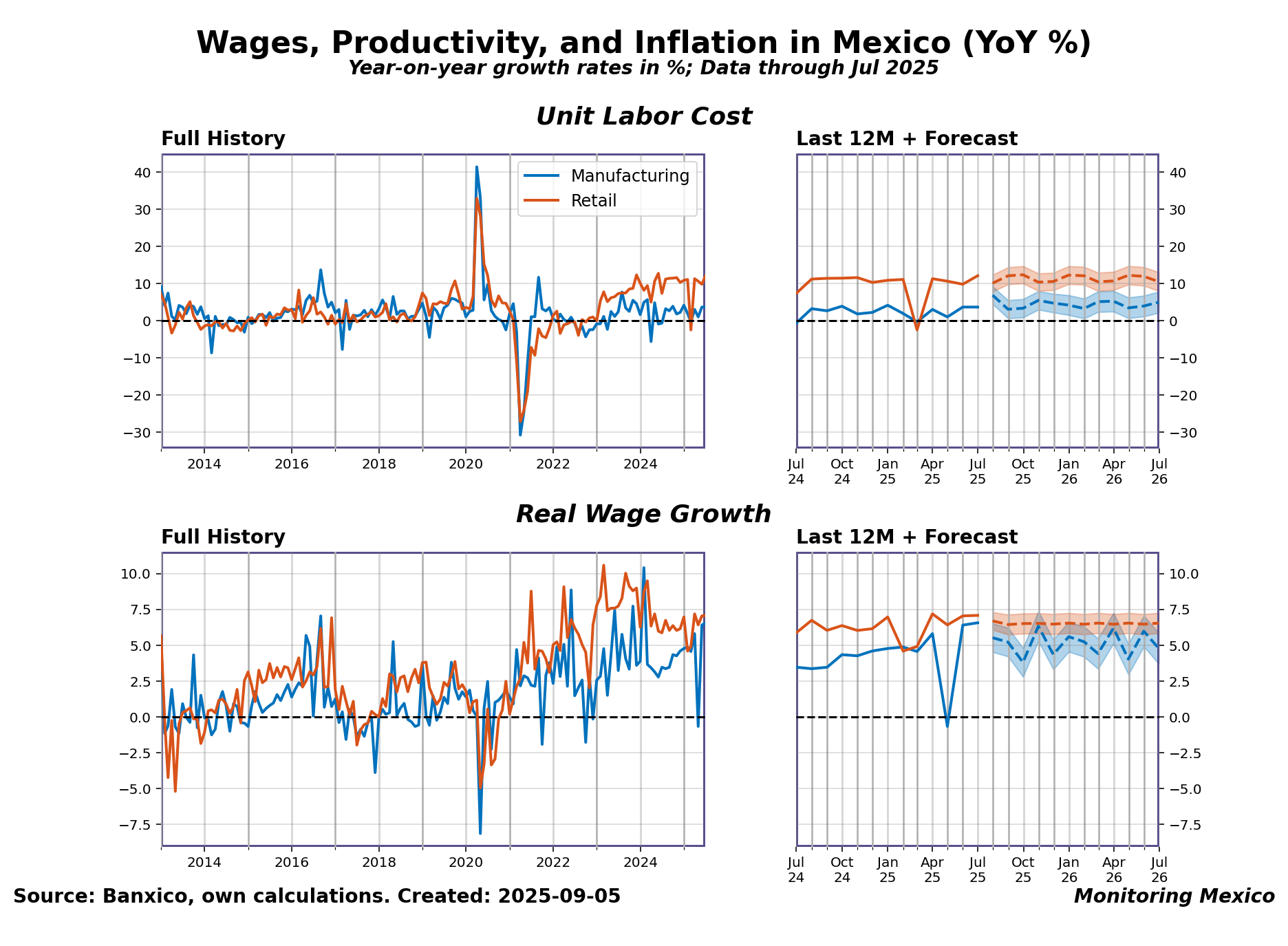

Nominal wages are rising faster than productivity, elevating labor costs. In July 2025, manufacturing unit labor costs grew by 3.69% year-over-year, near the 80th percentile, and retail ULC surged 12.1%, at the 97th percentile. Wage growth outstrips productivity gains, creating upward pressure on costs. Over the past year, the manufacturing ULC increased by 4.31%, while retail rose 4.75%. Exceptional volatility during the pandemic has subsided, but domestic cost pressures remain elevated. This wage-productivity gap signals continuing inflation risks as rising labor costs feed into prices.

Real wages continue to improve, but future gains face inflation uncertainty. Real wage growth in manufacturing stands at 6.57%, near the 98th percentile, with retail at 7.08%, both on upward trajectories. Inflation declines and policy measures supporting incomes have enhanced purchasing power recently. However, sustained inflation risks related to labor costs could erode these gains. The forecast suggests real wages may continue to outpace inflation short-term, supporting consumer demand, but volatility in underlying cost pressures warrants caution.

Sector disparities highlight domestic demand stresses and policy challenges. Retail sector wage growth and unit labor costs substantially exceed manufacturing, reflecting domestic market weaknesses versus export sector competitiveness. This divergence intensifies concerns about structural rigidities and market competition, which remain critically elevated. Policymakers face balancing inflation containment with maintaining real income growth amid uneven sectoral dynamics, underscoring the complexity of upcoming monetary decisions.

Labor costs and real wages shape Mexico’s inflation, competitiveness, and household demand. In Mexico, unit labor costs in manufacturing and retail capture how wage growth compares with productivity in key sectors exposed to both domestic demand and global competition. If costs rise faster than output, firms may raise prices, squeezing competitiveness and adding to inflation pressures. Real wage growth, on the other hand, reflects purchasing power: modest gains support household consumption, but in a country with high inequality and a large informal sector, many families see little benefit. For policymakers, these indicators are vital for balancing cost pressures, external competitiveness, and the fragile strength of domestic demand.

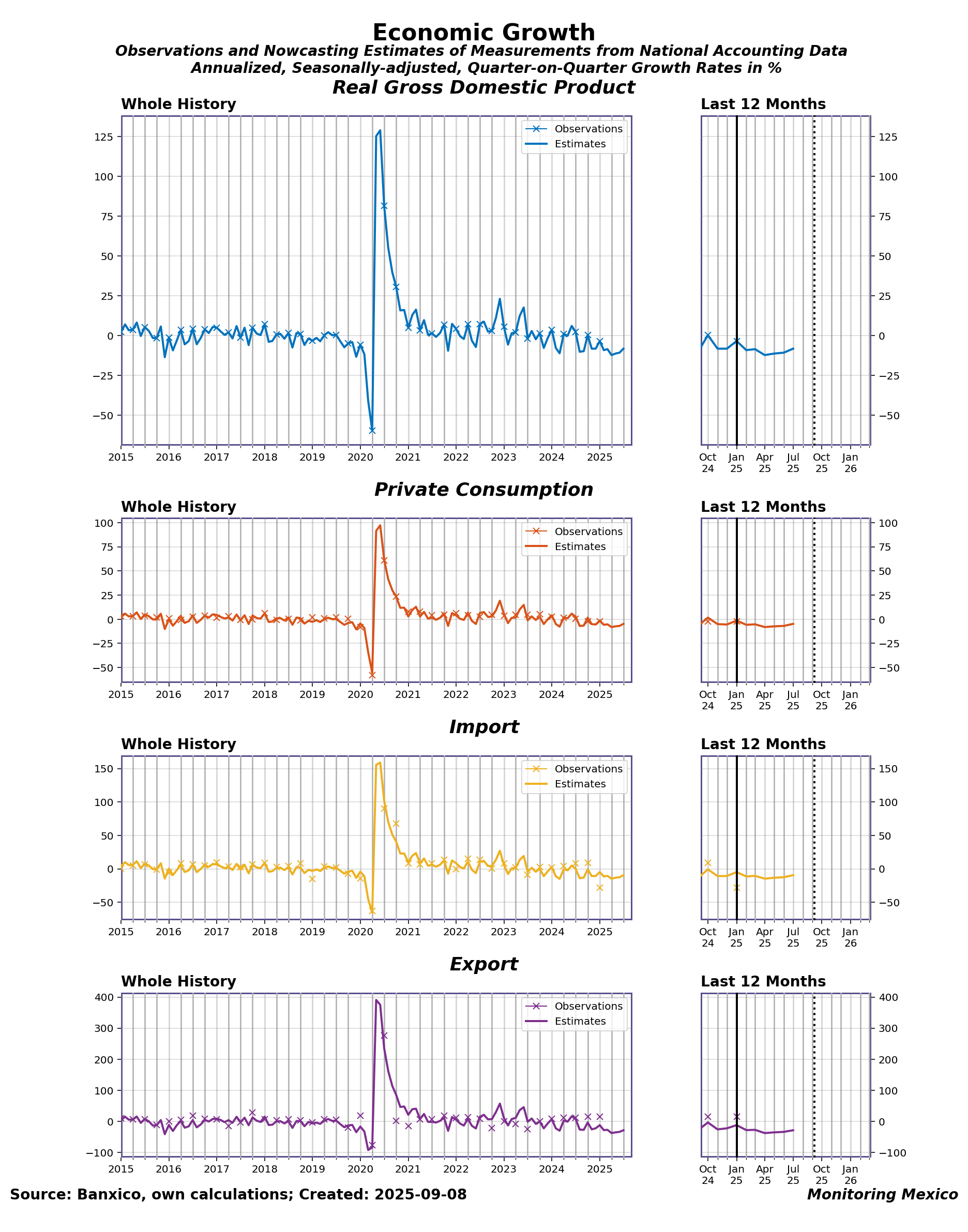

Real GDP growth exhibited modest recovery yet remains subdued at historical lows. Mexico's real GDP growth rate stood at -8.25% in July 2025, near the 13th historical percentile. Month-on-month, growth improved by 2.51 points though it declined by 10.5 points year-over-year. The economy is on a three-month upward trajectory but remains in a contraction phase, consistent with subdued capacity pressures. This ongoing weakness tempers expectations for immediate monetary policy easing despite recent rate cuts.

Private consumption remains a soft driver amid fragile household conditions. Private consumption growth registered -4.77% in July 2025, placing it in the 19th percentile historically. It showed a short-term improvement of 2.12 points compared to the prior month but contracted 7.49% annually. Consumption volatility is low, reflecting cautious household spending in light of restrained real income growth and savings. Consumption is thus a modest drag, restraining broader domestic demand recovery.

Exports display signs of stabilization amidst strained external demand. Exports declined by -28.7% in July 2025, at the 9th historical percentile, though they improved 5.23 points from the previous month. Year-over-year export contraction remains severe at -36.4%. External conditions are challenging with weakened demand in key markets and a neutral to slightly supportive exchange rate effect. Export trends remain a lagging indicator relative to broader GDP, signaling ongoing pressures on Mexico's external sector.

Import activity picks up slightly but remains far below historical norms. Imports fell by -9.4% in July 2025, near the 14th percentile historically. A three-month gain totaling 5.26 points contrasts with a 9.73% annual decline. This reflects subdued domestic spending and investment appetite alongside lingering supply-chain frictions. Import sensitivity to exchange rate movements is limited, consistent with cautious procurement practices.

Net trade contribution continues to weigh on GDP recovery prospects. The gap between exports and imports implies a negative net-trade contribution to GDP. Declining export performance amplifies the domestic slowdown, with no significant improvement in trade composition or terms of trade to offer relief. Net external balances thus constrain overall economic momentum.

Growing concerns about US policy shocks frame a cautious economic outlook. Overall demand shows tentative signs of stabilization but remains weak across all components. Exports and imports lag domestic indicators, reflecting external vulnerabilities amid heightened attention to US trade and monetary policy developments. Domestic demand, while improving marginally, is hampered by constrained consumption. The combined profile signals modest near-term growth, supporting a prudent policy stance with vigilance over international spillovers and persistent structural challenges.

Real activity data tracks the economy’s engine—output, spending, and trade—while nowcasts bridge the lag between releases. Real GDP captures total production; private consumption reflects household demand; exports and imports reveal external demand and the flow of inputs for Mexico’s trade-exposed, manufacturing-heavy economy. Shifts in U.S. demand, global prices, and the peso often show up first in trade, then filter into GDP and consumption. Because official series arrive with delays and revisions, model-based nowcasts provide an early, probabilistic read for policy timing—useful if treated with uncertainty bands and cross-checked against higher-frequency signals.

Mexico’s unemployment edges higher, pointing to tentative labor market slack. The national unemployment rate rose to 2.73% in July 2025, near the 17th percentile historically. It increased by 0.044 percentage points month-over-month and by 0.015 percentage points year-over-year, marking a three-month upward streak. Unemployment remains low by historical standards but its gradual rise signals caution about the business cycle’s momentum. This lagging indicator suggests that labor market adjustments are unfolding amid broader economic uncertainties.

Underemployment pressure softens slightly but shows signs of cyclical stress. The underemployment rate declined marginally to 7.57% in July, slightly above its historical median. Its volatility is low, but the recent uptick over six and twelve months points to lingering slack and persistent informal sector reliance, which strains overall economic dynamism.

Gender disparities in unemployment reflect sector-specific economic shifts. Male unemployment stands at 2.59% (8th percentile), stable over the year, while female unemployment rose to 2.77% (15th percentile), continuing an upward trend. Differences stem from sectoral exposures: male-dominated construction shows stability, whereas female-heavy services experience slower recovery. These diverging paths align with historical patterns of more persistent female unemployment.

Informal employment share reaches near-record high, underscoring structural fragility. Informal employment rose to 29.3% in July, ranking in the 98th percentile historically. This recent rise reflects ongoing weakness in formal sector job creation and greater sensitivity to regulatory and demand shocks. The high level signals a structural reliance on informal work, constraining productivity and social protection.

Unemployment duration trends suggest slowing reintegration into employment. Average unemployment spell length reached 1.85 quarters in April 2025, above its historical median, while the reintegration decay parameter hit a record 0.977, indicating a near-constant exit rate from unemployment. This suggests a diminished likelihood of quick reemployment as the hazard rate stabilizes, pointing to subdued labor market fluidity.

Advanced education among unemployed rises sharply, revealing a growing skill mismatch. The share of unemployed with advanced education climbed to a record 58.7% in April, while those with secondary education dropped to 28.8%, a historic low. This shift signals structural challenges, with higher-skilled workers facing disproportionate reintegration difficulties. These trends highlight the need for targeted policy on workforce training and placement to address evolving labor market demands.

Labor slack and its composition shape inflation pressure, policy timing, and social risk. Unemployment, underemployment, and unemployment by gender reveal how broad and uneven slack is; longer unemployment durations and weaker prospects for the more-educated raise scarring risks and damp wage growth. In Mexico’s large informal sector, the informal employment share can swing sharply—often contracting faster in downturns as unprotected jobs are cut first, then rebounding early—masking true slack if headline unemployment alone is tracked. For monetary policy, a wider, more persistent slack (especially among women and higher-education groups) tempers wage pressures and supports easing, while tightening is more defensible when duration shortens and formal jobs absorb workers. Tracking these dimensions helps distinguish cyclical slack from structural mismatches and calibrate the policy rate accordingly.

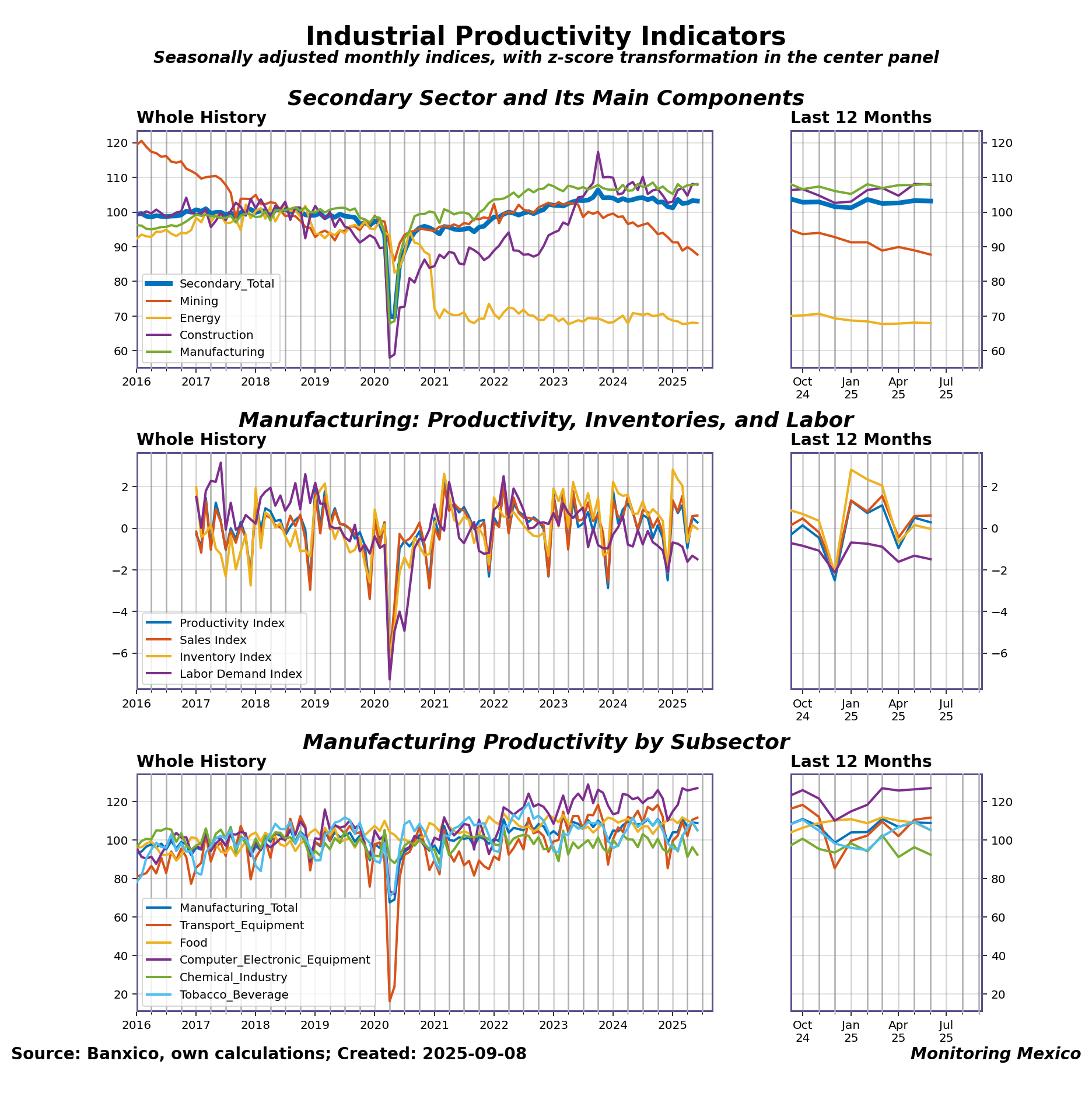

Mexico's secondary sector output remains robust but uneven across key industries. As of June 2025, the secondary sector's activity index stands at 103, near its 84th percentile historically. Month-on-month, it dipped slightly by -0.118, while year-on-year it contracted by -0.831. Manufacturing, which constitutes around 66% of the sector, remains the strongest performer with its index near the 99th percentile, whereas Mining and Energy subsectors show marked weakness, positioned near the 2nd and 5th percentiles respectively. Construction, at nearly 20% sector weight, remains elevated but posted a modest decline. The industrial outlook points to growth concentrated in select subsectors rather than broad-based expansion, raising concerns about resilience amid an uneven recovery.

Productivity gains contrast with mixed signals from sales, inventories, and labor demand. The manufacturing productivity composite index sits around the median at 0.281 growth, slightly down from the prior month. Sales growth has accelerated modestly to 0.61, reflecting some pickup in demand, yet inventory growth has turned negative, suggesting cautious production adjustments to avoid excess stock. Labor demand indicators declined sharply to the 8th percentile, signaling subdued hiring despite steady output, consistent with sustained efficiency gains. Divergent trends—stable productivity paired with falling labor demand and controlled inventories—imply current output levels may not yet translate into broad-based employment or signal a fully robust demand environment.

Productivity dynamics reveal sector-specific drivers within manufacturing. Manufacturing productivity index at 109 ranks in the 90th percentile, with a slight downtrend last month. Transport Equipment, the largest subsector at nearly 24% of manufacturing, shows significant productivity gains over two months, even as annual growth lags, while Computer and Electronic Equipment achieves near-record productivity levels, benefiting a substantial 9.8% manufacturing share. Conversely, Food and Chemicals, representing 18.6% and 6.3% respectively, report declines, reflecting sectoral headwinds. This mix highlights technological and efficiency improvements concentrated in capital-intensive industries versus cyclical or structural challenges in more traditional domains, suggesting uneven technical progress and potential vulnerabilities ahead.

Productivity trends reveal the economy’s capacity to grow without stoking inflation. In Mexico, productivity in the secondary sector—mining, energy, construction, and especially manufacturing—signals how efficiently output expands relative to inputs. Strong productivity gains mean firms can meet demand without raising prices, easing inflation pressure and supporting sustainable wage growth. Weak productivity, by contrast, constrains supply, making cost shocks more inflationary. Manufacturing deserves closer scrutiny, as its diverse subsectors respond differently to global demand, exchange rate shifts, and investment cycles. Tracking these patterns helps policymakers judge whether growth is supported by efficiency gains or reliant on credit and labor cost increases, shaping the space for monetary easing or tightening.

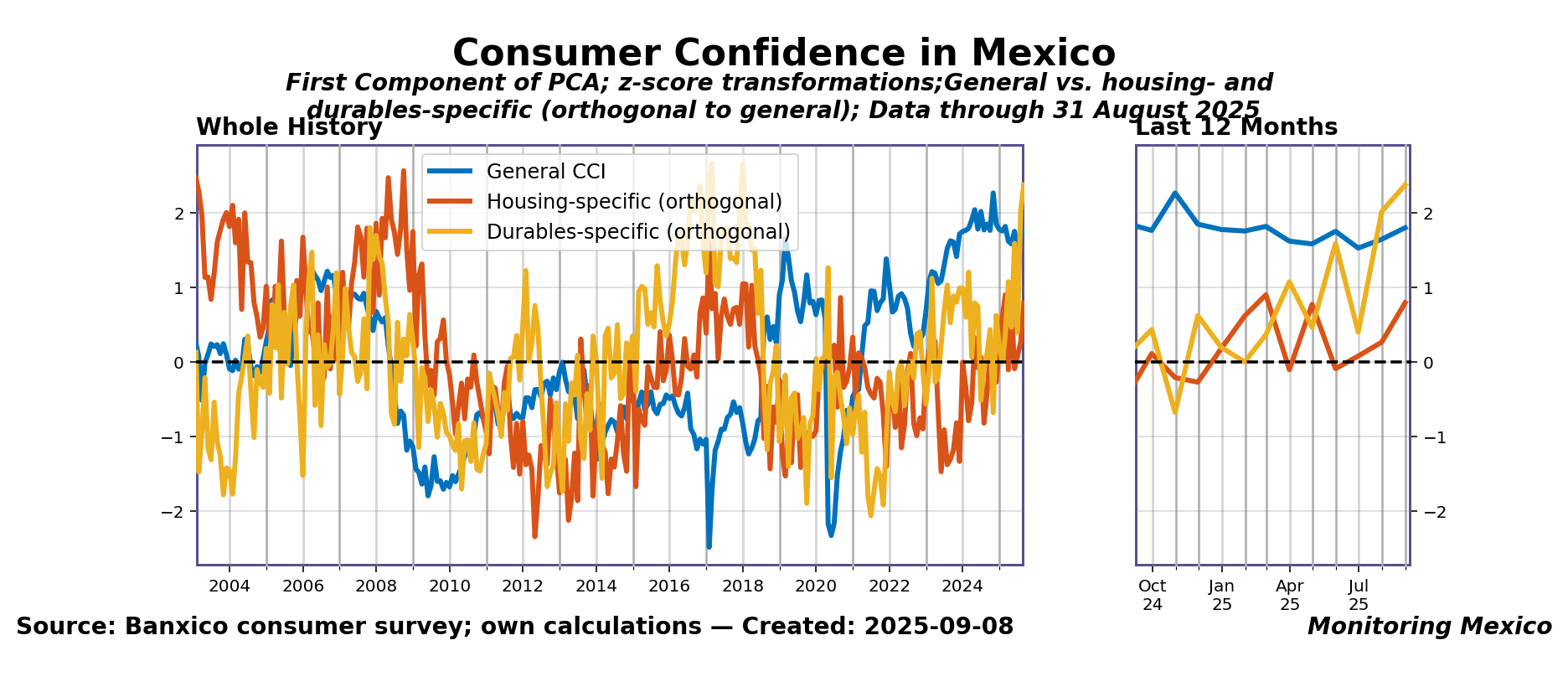

Mexican consumer confidence shows robust growth, driven by durable goods sentiment. In August 2025, the general consumer confidence growth rate rose to 1.8, near the 97th percentile, continuing a 2-month upward trend. Durable goods sentiment surged to a 2.38 growth rate, reaching the 99th percentile and marking a rare peak not seen in over seven years. Housing-specific confidence also climbed, hitting 0.793, but remains more modest by comparison. This divergence suggests stronger consumer appetite for high-value items, possibly supported by stable labor markets and real income gains amid a moderately high policy rate of 7.75%. However, housing remains cautious, reflecting persistent credit cost pressures and structural market constraints.

Consumer confidence captures households’ willingness to spend, a key driver of demand and inflation. Survey-based confidence indices gauge how secure households feel about their income and the economy. A general confidence index reflects overall sentiment, while targeted measures — such as willingness to buy durable goods or housing — reveal spending appetite in categories most sensitive to interest rates. Even if the technical construction is complex, the message is simple: stronger confidence supports consumption and can add inflationary pressure, while weaker confidence signals caution and slack. For monetary policy, these indicators help anticipate whether rate moves are restraining or stimulating household demand.

COMING SOON...

Aggregate concern among economists has moderately increased, reflecting rising unease. The Aggregate Concern Index for Mexico stood at 2.35 in August 2025, near the 56th historical percentile, marking gradual monthly and annual rises. It rose by 0.0228 on the month and 0.342 compared to a year ago, signaling a slow but steady build in caution. Recent volatility remains low, with the index only exceeding current levels twice in the past several months. This metric captures growing sensitivity among forecasters to evolving economic risks, suggesting a shift from complacency to heightened risk awareness. Such moderate elevation underpins a cautious tilt in monetary policy, balancing inflation control with growth concerns ahead of the September 25 meeting.

External policy shocks dominate, compounded by lingering structural challenges. Top concerns include US trade policy (index 20, 96th percentile) and public insecurity (16.3, 77th percentile), both maintaining elevated levels with sustained volatility. Other rule-of-law issues and domestic economic uncertainty hold mid-level risk with mixed recent trends. Domestic market weakness remains significant though slightly declined last month. The portfolio is increasingly shaped by external pressures, particularly US policies, alongside enduring governance and structural obstacles. These factors weigh on investment sentiment and suggest a tempered growth outlook, influencing expectations for policy continuity and caution in risk management.

Elevated recession risk underscores caution in the near term. The Anxious Index shows the perceived probability of recession at 40 (93rd percentile) comparing current versus previous periods, with a slight monthly rise. The next versus current perspective holds at 30 (91th percentile), stable but elevated. These readings reflect market apprehension about a slowdown, signaling downside risks to growth over coming months. Elevated recession fears likely constrain aggressive monetary easing, favoring precautionary messaging and measured rate decisions to manage inflation without undermining growth prospects.

Surveys of professional economists provide timely signals about emerging risks. While based on expert judgment rather than hard market data, these surveys are valuable because they capture informed views of where pressures may build next. Their timeliness offers policymakers and markets an early sense of shifting concerns before official statistics confirm the trend. As such, they serve less as precise forecasts and more as a risk map, highlighting areas that warrant closer monitoring.

Updated: 2025-09-01

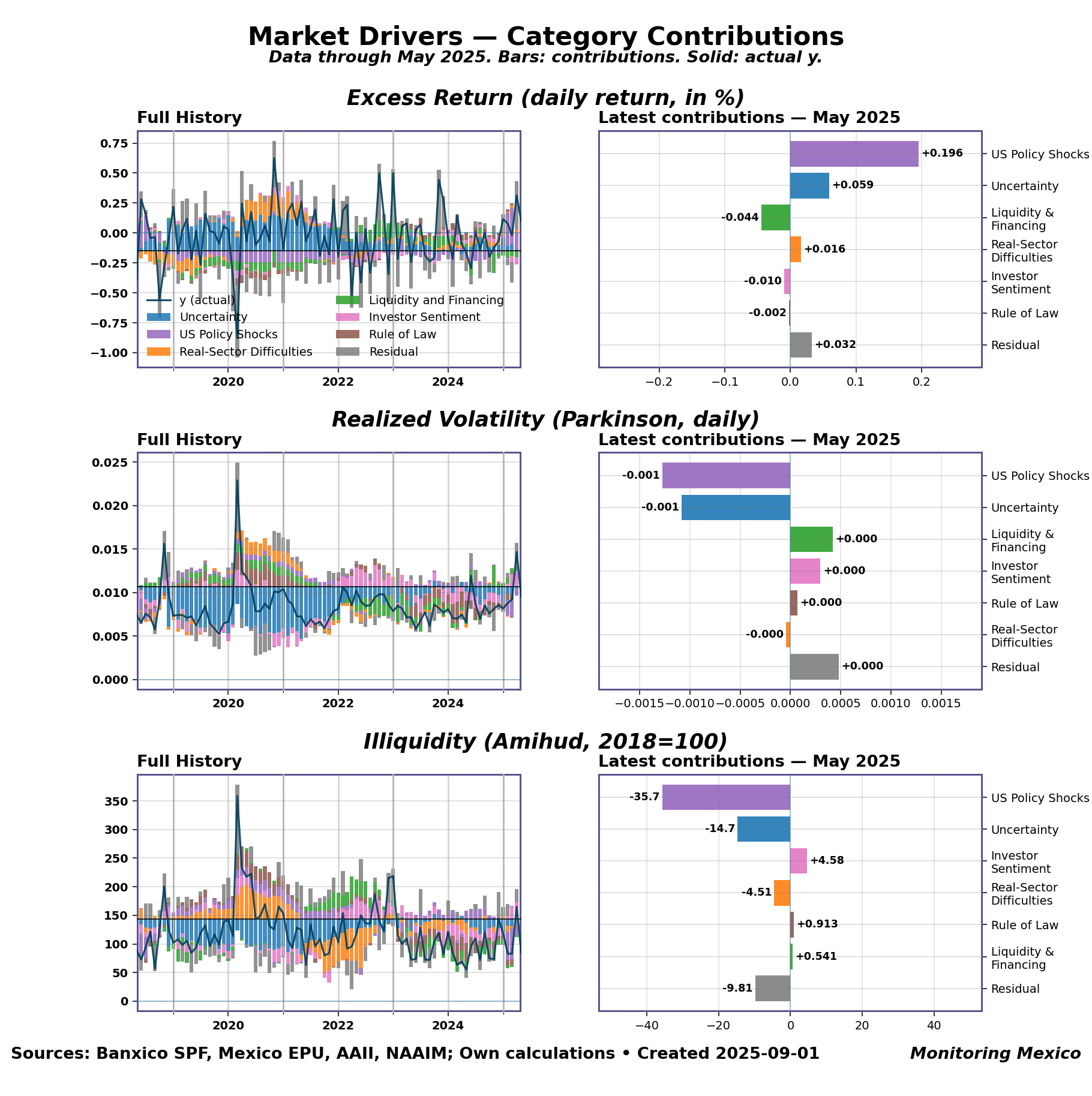

Market volatility metrics reflect a cautiously shifting risk landscape amid lingering structural challenges. As of May 2025, excess returns hover at 0.0988, aligning with the 72nd percentile yet down by 0.214 from the previous month. Realized volatility stands at 0.00955, near its 81st percentile, showing a similar monthly decline of 0.00513. Meanwhile, illiquidity dropped notably by 79.9 to 85.1, placing it at the 25th percentile, signaling improved market liquidity conditions. The preceding year saw volatility spikes and dips intertwined with global policy shocks and market uncertainty. This environment implies a tentative risk appetite with funding conditions modestly easing, though price discovery remains sensitive to shifts in structural dynamics and external influences.

Macro factors driving recent market moves continue to center on external and domestic pressures. US policy shocks, including trade and monetary policy, alongside uncertainty and liquidity concerns, consistently dominate volatility’s contribution. Recent months highlight a rise in structural constraints and competition issues, surging to extreme levels and amplifying market apprehension. While liquidity showed some improvement, underlying frictions persist due to regulatory and competitive deficiencies. This blend of persistent external shocks and intensifying internal structural challenges complicates Mexico's monetary and financial stability outlook.

Sentiment and uncertainty indicators reveal a market wrestling with fundamental concerns amid easing short-term risks. Investor sentiment, reflected in confidence spreads and exposure metrics, shows cautious positioning without excess optimism or panic. The Economic Policy Uncertainty index signals elevated, yet stable, policy-related stress, underscoring market participants’ wariness about deeper economic reforms and competitiveness. These factors feed into the moderate volatility and improved liquidity marks observed, but any resurgence in structural doubts or adverse policy surprises could amplify volatility sharply. The coming weeks likely hinge on policy clarity and tangible progress on structural reforms to temper unease and support market stability.

Financial market returns, volatility, and liquidity signal investor sentiment and risk appetite. Excess returns over government bonds capture the risk premium investors demand for holding equities; wider spreads suggest higher perceived risk or stronger growth prospects. Realized volatility in a stock market index reflects uncertainty — sharp swings indicate fragile sentiment and raise the cost of capital. Illiquidity, measured in the spirit of Amihud, shows how trading volume and price impact interact: when liquidity dries up, small trades can move prices disproportionately, amplifying shocks. For monetary policy, these indicators matter because they shape funding costs, investment flows, and the broader transmission of rate decisions into financial conditions.

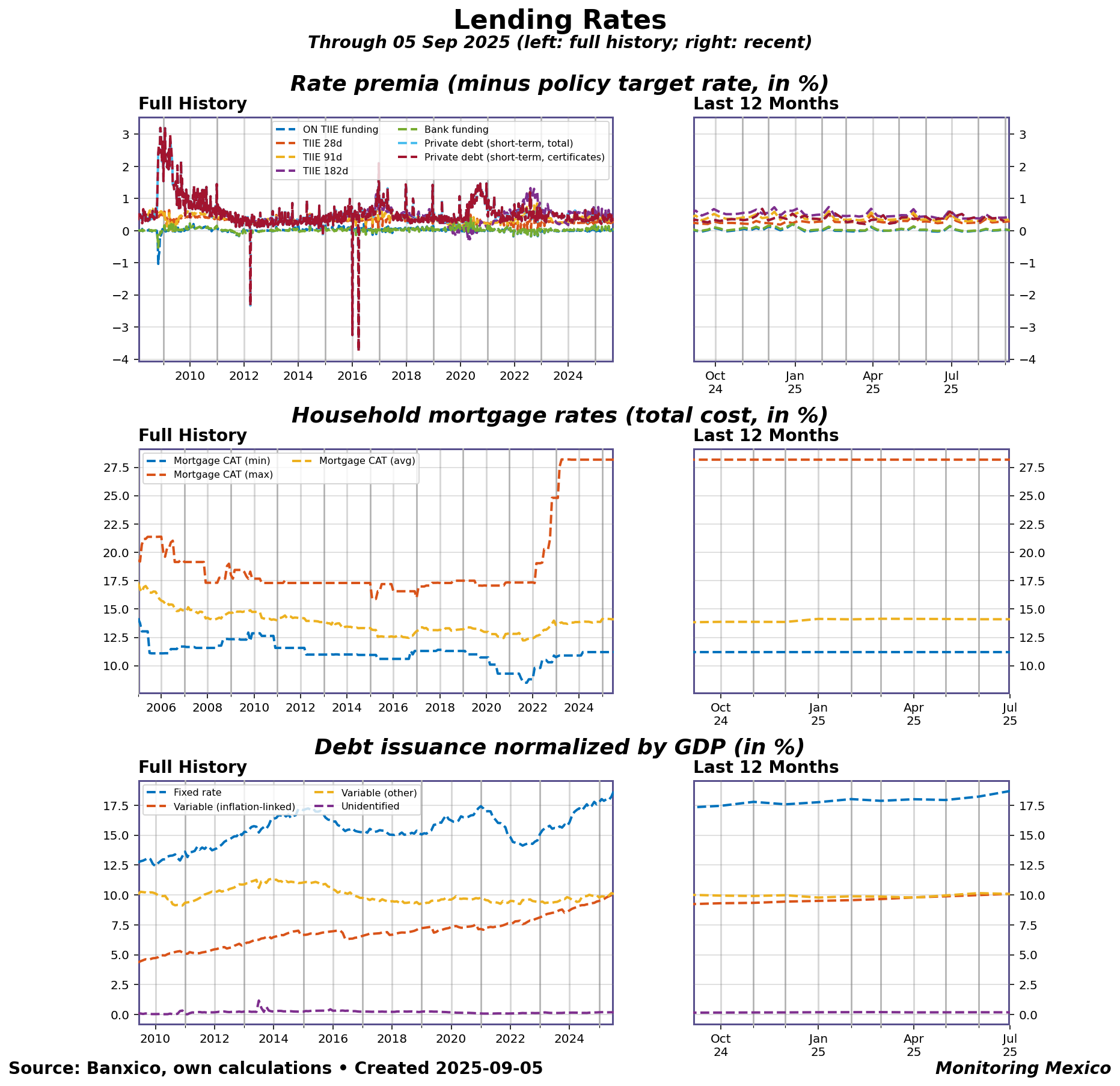

Funding premia have narrowed recently, reflecting improved liquidity conditions despite ongoing policy challenges. Current spreads show the ON TIIE funding premia close to 0.01 percentage points, with short-term TIIE rates at roughly 0.29 to 0.43 points above policy. These premia have steadily narrowed over the past five months, indicating easing liquidity stress. The term structure remains upward sloping, suggesting modestly higher rate expectations over longer horizons. Private debt and bank funding premia align with this trend, highlighting gradual normalization following prior tightening episodes. Overall, financial conditions indicate less acute market strain, yet underlying uncertainty persists due to external shocks.

Mortgage rates remain elevated relative to policy, constraining affordability and household credit growth potential. Mortgage CAT rates currently range from 11.2% to 28.18%, with an average of 14.1%, notably above the 7.75% policy rate. This lagged pass-through reflects persistent credit costs that continue to weigh on borrower affordability. The stable average CAT over recent months suggests limited near-term easing in household borrowing costs. Consequently, mortgage credit expansion is likely to remain restrained, maintaining downward pressure on domestic demand dynamics.

Debt issuance relative to GDP hits record highs, increasing exposure to interest-rate risk amid elevated external uncertainty. Debt issuance now stands at a historical peak of 39.1 per 1,000 GDP, with fixed-rate instruments dominating at 18.7 and variable inflation-linked instruments close behind. The substantial share of inflation-linked and variable debt heightens exposure to inflation and rate volatility. Recent increases in issuance reflect heightened market funding needs amid evolving financing conditions. This elevated debt burden, combined with growing concerns over US policy shocks, underscores vulnerability to shifts in global monetary policy and trade dynamics.

Lending rates link monetary policy to households, firms, and financial markets. Rate premia show how market and bank funding costs move relative to the policy rate, indicating the efficiency of monetary transmission. Household mortgage rates capture the cost of long-term borrowing; their sharp rise in recent years signals affordability pressures and distributional effects, as many families face double-digit costs. Debt issuance patterns, normalized by GDP, reveal how firms finance themselves — the balance between fixed and variable rates matters for vulnerability to policy shifts. Together, these indicators show how policy rates filter into real borrowing conditions, affecting credit demand, investment, and ultimately growth and inflation dynamics.