Stay informed with the latest insights on Mexico's economy via statistics, AI analysis, and synthesis.

Today's Lead:

Monetary Policy — Market Expectations: new observations

Financing — Nonfinancial Lending: new data and revisions (higher)

Financing — Volatility: data revised lower

Updated: 2026-08-11

Miguel Mancera Aguayo, the first governor of Mexico's central bank, Banxico, has passed away at the age of 93. His contributions to the financial sector and his role in shaping monetary policy in Mexico are recognized as significant. The news of his death has prompted reflections on his legacy in the banking community. — El Financiero, 11 Aug 2026. Read more

Inflation in July reached its lowest level in four years, primarily driven by decreases in agricultural and energy prices. This decline marks a significant shift in the economic landscape, reflecting changes in these key sectors. — El Economista, 11 Aug 2026. Read more

The price of gold is approaching a seven-week high, driven by a weaker dollar and rising geopolitical tensions. Investors are closely monitoring the situation as it influences market dynamics. Analysts suggest that these factors are contributing to the increased demand for gold as a safe-haven asset. — El Economista, 11 Aug 2026. Read more

Global stock markets experienced slight declines on Monday, influenced by ongoing tensions in the Middle East. Investors are closely monitoring the situation, which has raised concerns about potential economic repercussions. The article highlights the cautious sentiment among traders as geopolitical developments unfold. — El Economista, 11 Aug 2026. Read more

Colombia recorded an inflation rate of 0.17% for the month of July. This figure reflects the changes in consumer prices during that period, indicating a slight increase in inflation compared to previous months. The report highlights the ongoing economic conditions affecting the country. — El Economista, 11 Aug 2026. Read more

The Mexican peso has achieved its best level against the dollar since February, gaining 1.05% over the week. This improvement is attributed to a weaker dollar, which has influenced the exchange rate positively for the peso. — El Economista, 07 Aug 2026. Read more

Young individuals are reportedly accumulating up to five credit cards, while banks are reducing their credit placements. This trend highlights a shift in consumer behavior among the youth, as they seek to manage their finances through multiple credit options despite the tightening of credit availability by financial institutions. — Expansión, 07 Aug 2026. Read more

Mexican banks earned 149,120 million pesos in the first half of the year, marking a 5.4% decline compared to the previous year. This decrease highlights ongoing challenges within the banking sector amid changing economic conditions. — El Economista, 07 Aug 2026. Read more

The Mexican peso has recorded three consecutive days of gains against the US dollar, closing at 17.20 units. This positive trend reflects the currency's strengthening performance in the foreign exchange market. — El Financiero, 06 Aug 2026. Read more

The article explores the impact of inflation on personal finances, emphasizing its role as a significant concern for individuals. It discusses how rising prices affect purchasing power and savings. The piece includes insights from financial experts who highlight the need for effective strategies to manage inflation's effects on household budgets. — El Financiero, 06 Aug 2026. Read more

Has Mexico reined in its inflation rate? Not yet, says Banxico chief — Google News, 10 Aug 2026. Read more

Mexican Peso Rally Stalls As Markets Await US Inflation Data — Google News, 10 Aug 2026. Read more

Mexican Peso rally pauses ahead of US inflation report — Google News, 10 Aug 2026. Read more

Dollar Remains Below 18 MXN: What Is the Exchange Rate Today, Sunday, August 9, 2026? — Google News, 09 Aug 2026. Read more

Borderlands Mexico: USMCA gives Mexico an edge as global trade barriers rise — Google News, 09 Aug 2026. Read more

Updated: 2026-08-08 by María López

Key Takeaways

Following the May 7, 2026 decision, Banxico's policy rate stands at 6.50%. After Banxico's May 7 meeting, the target rate remains unchanged, reflecting a cautious approach amid rising global inflation and domestic economic challenges. This marks a streak of zero changes since the last cut of 0.25% earlier this year, indicating a careful balance as policymakers weigh immediate economic stability against longer-term structural reforms. The cumulative change over the current cycle points to a determined effort to maintain price stability despite external pressures.

Relative to the United States, the Fed's target rate is at 3.62%, creating a notable differential of 2.88%. The Fed's recent decisions have shown a pattern of holding rates steady, with their latest cut occurring back in December 2025. This first-mover advantage for the Fed highlights a divergence in monetary policy paths, as Banxico grapples with local economic conditions while the Fed remains focused on its own inflationary challenges.

The rate differential is likely to impact capital flows significantly. For markets, this gap could amplify pressures on the MXN/USD exchange rate, as investors may seek higher yields in Mexico while weighing the risks associated with domestic security and policy uncertainty. This dynamic adds further complexity to Banxico's decision-making landscape as it navigates both local and external economic pressures.

The central bank's policy rate is the primary tool for steering inflation and economic activity. Banxico targets 3% annual inflation and adjusts its overnight interbank rate to influence borrowing costs throughout the economy. The rate differential with the United States affects capital flows and exchange rate dynamics — a wider spread can attract foreign investment but may constrain domestic credit. Policy decisions are announced roughly every six weeks following scheduled monetary policy meetings.

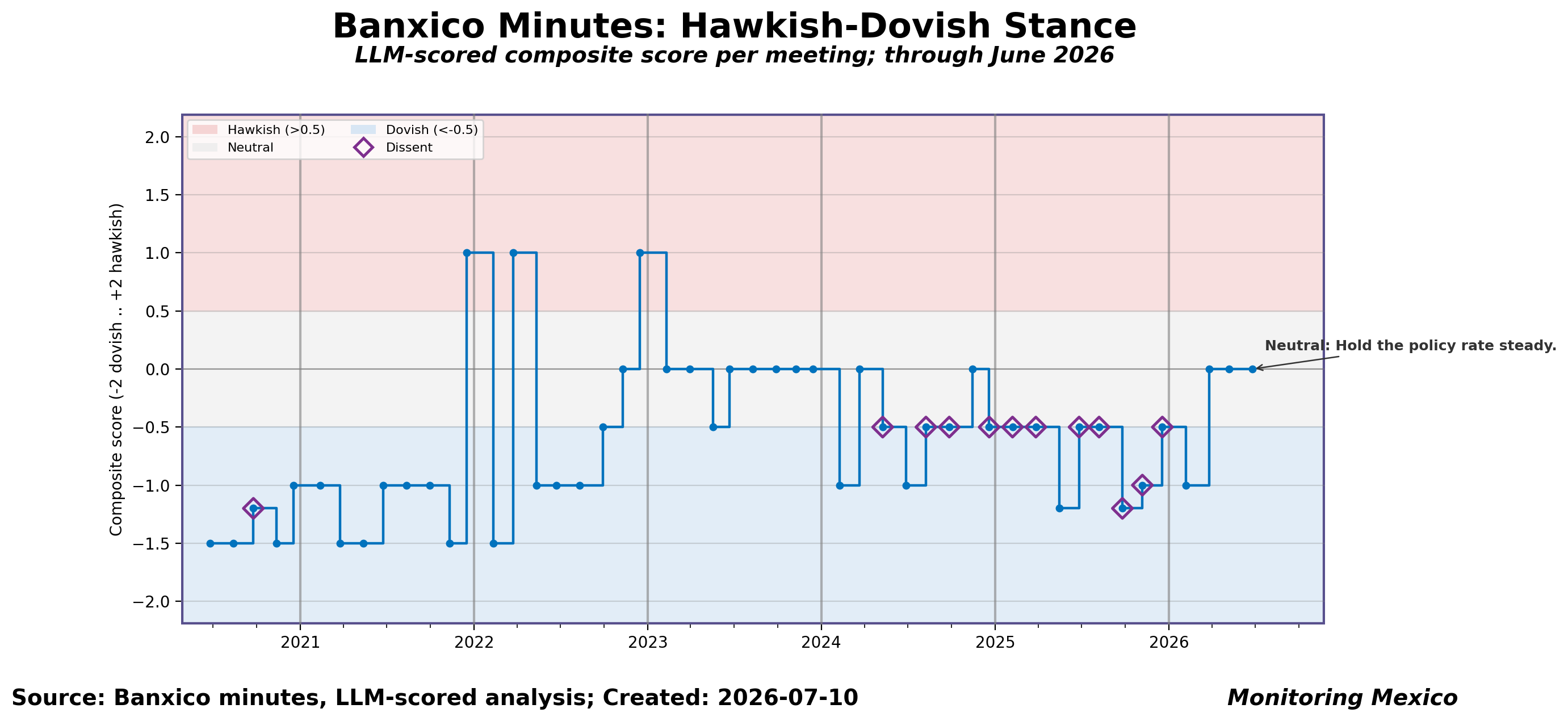

Updated: 2026-07-10 by María López

Key Takeaways

Banxico's minutes from the June 25 meeting show a neutral tone (composite score +0.0). Banxico's minutes from the June 25 meeting show a neutral tone (composite score +0.0). The committee's decision: Hold the policy rate steady.. Vote split: 5 hold.

The committee emphasizes the commitment to price stability. Forward guidance: The committee emphasizes the commitment to price stability. Future policy will be data-dependent, with a focus on inflation dynamics and external risks. Hawkish signals: Global inflation continues to rise due to energy prices.; Inflation expectations for the end of 2026 have been revised upwards in various countries.. Dovish signals: Recent negotiations have eased concerns about energy supply.; The US labor market risks have decreased, with stable job creation..

The tone is more hawkish compared with the prior 3 meetings. The tone is more hawkish compared with the prior 3 meetings. The latest composite score of +0.0 compares with a -0.3 average over the previous 3 meetings. The vote was unanimous, with no recorded dissent.

Each Banxico monetary policy meeting's published minutes are analyzed by a large language model, which scores the committee's overall tone on a composite scale from -2 (very dovish) to +2 (very hawkish) and extracts the vote split, forward guidance, and hawkish/dovish signals. Minutes are typically published by Banxico about two weeks after the corresponding policy decision, so this analysis always lags the live decision by that margin. The commentary on this page is assembled directly from those stored, structured fields rather than generated by a separate LLM call.

Updated: 2026-08-11 by Ignacio Crane

Key Takeaways

With recent adjustments to inflation expectations and heightened economic policy uncertainty, our model-based expectations indicate a substantial chance of no action from Banxico at its upcoming meeting on February 5, 2026. The current expected change from the model suggests an anticipated mean adjustment of -11bp, reflecting a modal bucket probability of ±0bp at 58.0% and a secondary probability of -25bp at 38.9%. This marks a material shift from our previous assessment, where the modal bucket was at -25bp. The data points toward likely inaction amidst a backdrop of declining headline inflation and rising uncertainties surrounding economic policies.

Recent inputs from key economic drivers reveal notable shifts that could influence Banxico's decision-making process. Notably, inflation data has shown a modest deceleration, while economic policy uncertainty has intensified. These updates align with the prevailing sentiment in the market and underscore the dynamic nature of the current economic landscape.

The interplay of these drivers suggests a complex decision-making environment for the central bank. Moderate dovish pressure arises from the declining inflation, while the escalating economic policy uncertainty exerts a slight hawkish pull. Particularly, the rising economic policy uncertainty has become a significant concern for policymakers, overshadowing other factors. It is crucial to note that while some drivers exert influence, the actual decision will ultimately depend on the committee's judgment, rather than merely the mechanics of our model.

Ordered Probit Probabilities

| Rate Change | 04 Feb | 05 Feb 2026 | Δ |

|---|---|---|---|

| Cut | 58.4% | 42.0% | -16.4 |

| Hold | 41.6% | 58.0% | +16.4 |

| Hike | 0.0% | 0.0% | +0.0 |

| E[Δrate] | -17.5 bp | -11.3 bp | +6.2 bp |

Probabilities in %. Modal bin in bold. E[Δrate] = probability-weighted expected change in basis points.

When markets and the public can anticipate how and why the central bank acts, uncertainty falls and policy becomes more effective. Clear communication helps businesses plan investments, households make borrowing decisions, and international investors gauge currency risks. Economists often stress the importance of clarity and traceability — the ability to follow and understand decisions step by step. Without it, rate moves risk being misread, causing volatility instead of stability. With it, policy signals are more credible, anchoring expectations and strengthening the central bank's influence.

Rate-change probabilities are estimated using an ordered probit model with eight macroeconomic and financial drivers: consumer price inflation (CPI), consumer confidence, the 30-day peso/dollar change, the CETES 28-day spread, stock market growth, the yield curve slope (10Y minus 2Y), Mexico's Economic Policy Uncertainty index, and the Fed-Banxico rate differential. The model maps these drivers into probability bins for the next monetary policy decision, ranging from cuts of 50 basis points or more to hikes of the same magnitude. Coefficients are estimated on the historical record of Banxico decisions and their pre-decision data environment. Probabilities update daily as driver series refresh and should be treated as one input among many.

Out-of-sample backtest across 24 past meetings: the modal prediction matched the actual decision 46% of the time, directional accuracy (hike/hold/cut) was 67%, Brier score 0.720. Out-of-sample backtest across 24 past meetings: the modal prediction matched the actual decision 46% of the time, directional accuracy (hike/hold/cut) was 67%, Brier score 0.720. Lower Brier scores indicate better-calibrated probability forecasts.

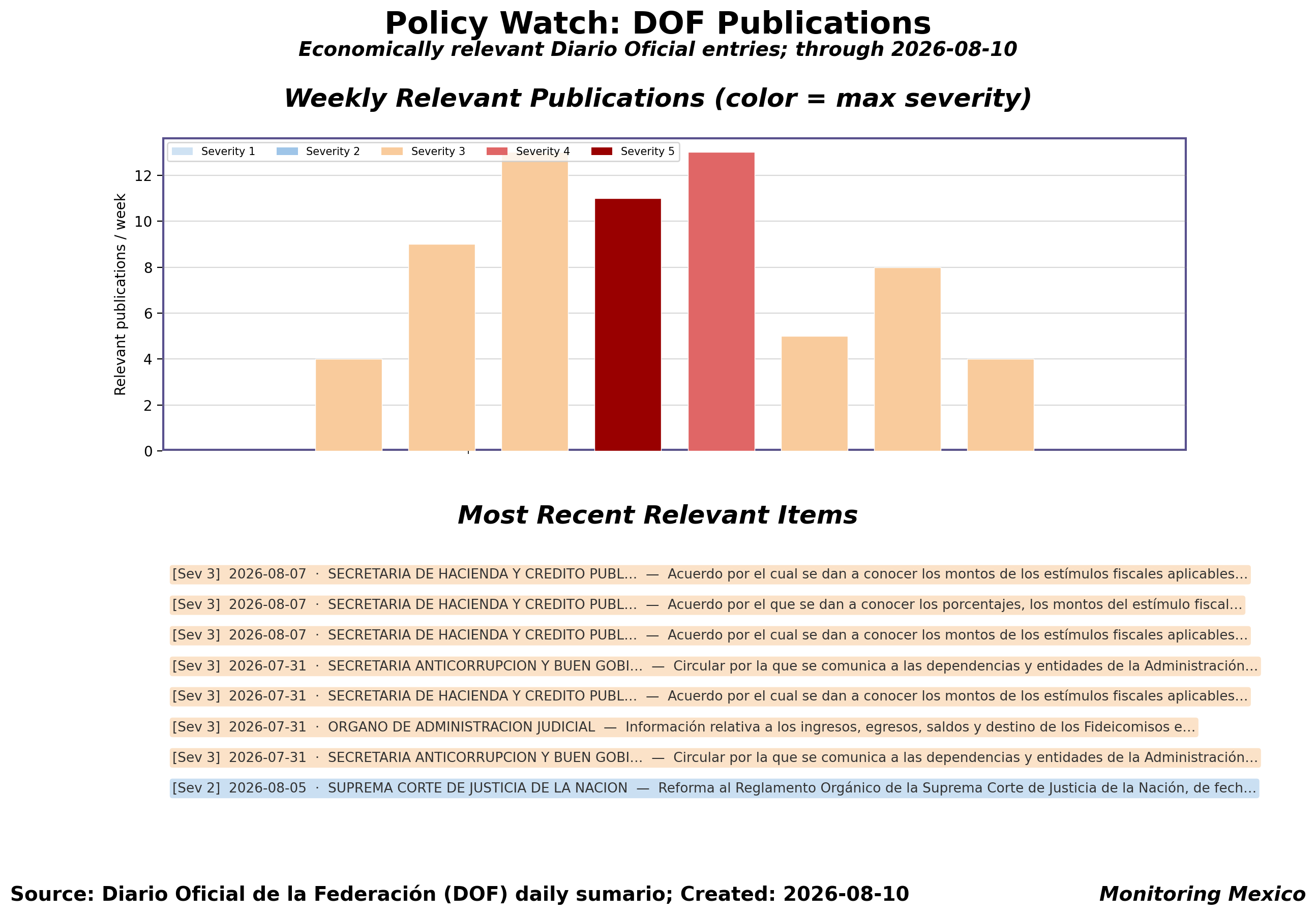

Updated: 2026-08-10 by Pablo Rivas

Key Takeaways

The DOF carried 4 economically relevant publications in the week ending August 10, 2026. The DOF carried 4 economically relevant publications in the week ending August 10, 2026. By category: tax (3), trade (2), judicial (1), energy (1). The weekly maximum severity reached 3/5.

Recent notable publications include:. August 07 — SECRETARIA DE HACIENDA Y CREDITO PUBLICO: Acuerdo por el cual se dan a conocer los montos de los estímulos fiscales aplicables a la enajenación de gasolinas en la región fronteriza… (severity 3/5). August 07 — SECRETARIA DE HACIENDA Y CREDITO PUBLICO: Acuerdo por el que se dan a conocer los porcentajes, los montos del estímulo fiscal y las cuotas disminuidas del impuesto especial sobre pr… (severity 3/5). August 07 — SECRETARIA DE HACIENDA Y CREDITO PUBLICO: Acuerdo por el cual se dan a conocer los montos de los estímulos fiscales aplicables a la enajenación de gasolinas en la región fronteriza… (severity 3/5).

CONAMER (the Comisión Nacional de Mejora Regulatoria), which previously required draft regulations to be pre-published for public consultation before taking effect, was extinguished by a reform enacted in June 2025. With that pre-publication consultation step gone, the Diario Oficial de la Federación is now the earliest official signal available for new regulations, decrees, and reforms — there is no longer an upstream draft-stage checkpoint to monitor instead.

This monitor scans the DOF's daily sumario (official gazette summary) for publication titles and issuing organisms, then applies a keyword classifier — not an LLM — to flag economically relevant entries across six categories (tax, trade, labor, energy, financial regulation, judicial) and assign a severity score from 1 (routine) to 5 (major fiscal/labor policy change, e.g. Miscelánea Fiscal or a minimum-wage decree). Only sumario titles and issuing organisms are scanned in this MVP; full document text is not retrieved or analyzed.

So…what is this—and why am I doing it?

This project began with a simple question in 2021: how much of the work of producing useful economic information can we hand over to machines? Monitoring Monetary Policy in Mexico is a thought experiment at that frontier. By combining statistical analysis, tailored visualizations, and large language models, it demonstrates how even highly specialized topics—such as Mexican monetary policy—can be made more accessible, relevant, and insightful. Meanwhile, the system is designed to run without human intervention on a daily basis. My role is to set the design; the automation carries it out.

When does data stop being a dump and start being a story?

The initiative builds on my earlier Monitoring Mexico project but has since evolved in important ways. Data is no longer simply displayed; it is analyzed, distilled, forecasted, visualized, interpreted, narrated, and contextualized. Large language models help transform both raw and modeled data into context, turning numbers into stories. In short, raw information is transformed into understanding.

Who’s in charge here—a Raspberry Pi or common sense?

Behind the scenes, the site runs on a Raspberry Pi 5 powered by Python and a library of custom routines. Automation drives much of the process, but human expertise remains essential in designing the explanation and presenting the material. The balance between machine efficiency and human judgment is what makes the project work.

How do we cut through the jargon and keep the signal?

The aim is straightforward: to bring clarity to an area often obscured by technical detail. Monetary policy shapes households, firms, and markets, yet its analysis usually remains confined to experts. By filtering, explaining, and visualizing the data, this project seeks to make that knowledge more transparent and more useful.

Is this the 80/20 rule you learn in business school in the wild?

At its core, the site is both a contribution to public understanding and an exploration of how informational value is created. It is a humble attempt to deliver 80% of the insights of a central bank analysis with 20% of the resources—while also testing what the future of knowledge generation might look like.

What might be new the next time you drop by?

This is very much a work in progress, with new features, analyses, and visualizations added over time. We can now at the brink of generating our very own economic policy uncertainty (EPU) index, and we consider a newsletter. But maybe a chatbot might be more appropriate? Coming back to check for updates is always a good idea. If the site sparks curiosity, fosters dialogue, or simply helps illuminate Mexico’s economic dynamics, it has achieved its goal.

Updated: 2026-08-08 by María López

Key Takeaways

The mid-July 2026 CPI release shows headline inflation at 3.38%, comfortably nestled within Banxico's 2%-4% target band. This figure marks a slight uptick of 0.04% from the previous release, suggesting a modest upward trend in consumer costs. While it’s good news that we’re under the target, it’s crucial to recognize that the latest reading is still near the 22nd percentile historically, indicating that inflationary pressures are not entirely subdued. This modest increase could signal to policymakers that while we’re stable for now, underlying cost dynamics remain a concern.

Core inflation, which excludes volatile food and energy prices, paints a different picture. At 4.05%, core inflation is elevated and sits above the target, reflecting persistent price pressures that aren’t just a temporary blip. Although it dropped slightly by 0.000749% from the prior month, it remains 1.05% above Banxico’s target, highlighting a divergence from headline inflation trends. This discrepancy suggests that while headline figures might appear manageable, the underlying inflationary landscape is more troublesome, complicating the central bank's policy path.

Trade prices are telling a different story, with export prices remaining stubbornly high. The latest data shows export prices at 12.84%, significantly above historical norms, which could signal ongoing inflationary pressures linked to international markets. Meanwhile, import prices at 5.43% also reflect a strong upward trajectory, albeit less pronounced than export trends. These dynamics underscore the interconnectedness of domestic inflation with global supply chain challenges, posing a dilemma for Banxico as it contemplates future rate adjustments.

| 2H Jul 2026 | 2H Jul 2027 | |||||

|---|---|---|---|---|---|---|

| Series | Current | Prev. Fcast | Error | 12M Fcast | Prev. 12M | Rev. |

| Headline CPI | 3.4 | — | — | 4.6 | 4.6 | +0.00 |

| Core CPI | 4.0 | — | — | 4.4 | 4.4 | +0.00 |

| Export Price Index | — | — | — | 5.7 | 5.7 | +0.00 |

| Import Price Index | — | — | — | 5.0 | 5.0 | +0.00 |

All values in percentage points (YoY, seasonally adjusted). "Error" = actual minus previous forecast. "Revision" = change in 12-month outlook since last update. "—" = no prior forecast available.

The Consumer Price Index (CPI) measures changes in the cost of a representative basket of goods and services purchased by Mexican households. Banxico targets 3% annual inflation with a tolerance band of 2%-4%. Core CPI — which excludes volatile food and energy prices — reveals underlying inflation trends that guide monetary policy. Import and export price indices extend the picture by linking Mexico's inflation dynamics to global markets, trade flows, and currency movements.

Headline CPI, core CPI, export prices, and import prices are projected six months ahead using a Vector Autoregression (VAR). The four series are estimated jointly, so each informs the others' forecasts through lagged interactions. Projections update each time new CPI data arrive and may shift materially after revisions.

Out-of-sample backtest over 72 evaluation windows using the Vector Autoregression (VAR). Out-of-sample backtest over 72 evaluation windows using the Vector Autoregression (VAR). RMSE measures the typical forecast error in the same units as the series; 'naive' is a no-change benchmark. Headline CPI (RMSE 1.07 vs 1.02 naive, n=72); Core CPI (RMSE 0.64 vs 1.05 naive, +39% improvement, n=72); Export Price Inflation (RMSE 7.27 vs 7.77 naive, +6% improvement, n=56); Import Price Inflation (RMSE 2.99 vs 2.05 naive, n=56).

Updated: 2026-06-26 by Alexander Dentler

Key Takeaways

The recent update from the SHF House Price Index reveals significant insights into the state of the housing market, particularly with the new observation of 8.71% YoY inflation as of 2026-01-01. This level of house price inflation exceeds historical averages, positioning itself in the 75th percentile since 2006. In comparison, headline CPI inflation stands at 3.94% while housing CPI inflation is at 3.61%, suggesting that house prices are rising notably faster than general inflation metrics. This divergence reflects the ongoing demand pressures in the housing sector, despite a slight decline of 0.21 percentage points from the previous quarter.

The DFM nowcast provides valuable context, estimating house price inflation at 8.65% YoY as of 2026-05-01. This nowcast aligns closely with the latest observed value, indicating that auxiliary indicators such as mortgage lending and housing CPI are confirming the current trajectory rather than suggesting any significant upward or downward pressure. The model's consistency with observed data suggests that the dynamics within the housing market remain robust and supportive of sustained inflationary trends.

DFM Nowcast Comparison

| Observed | Nowcast | Prev. Nowcast | Gap | Revision | |

|---|---|---|---|---|---|

| SHF House Price Inflation (YoY) | 8.71% | 8.65% | 8.65% | -0.06 | +0.00 |

Observed: 2026-Q1. Nowcast: 2026-05. Previous nowcast: 2026-05. "Gap" = nowcast − observed. "Revision" = change in nowcast since previous run.

The SHF House Price Index is published quarterly by Sociedad Hipotecaria Federal, Mexico's federal mortgage development bank, typically around 40 days after the reference quarter ends. It is constructed from mortgage appraisal data (avalúos) using a Case-Shiller repeat-sales methodology, with breakdowns by state, new vs. used housing, and market segment (affordable vs. mid-to-high-end). Because the index reflects prices at the point of mortgage origination, it captures credit-driven demand rather than asking prices, making it a tighter gauge of actual transaction values and collateral quality across the housing market.

A Dynamic Factor Model (DFM) filters the quarterly SHF House Price Index using five Banxico auxiliary series — the funding rate, mortgage lending volumes, a housing purchase survey indicator, the SPF unemployment forecast, and construction activity — plus two CPI components (headline and housing subcategory). The model extracts a common factor from these seven indicators, producing a smoothed nowcast that updates between quarterly SHF releases whenever auxiliary data arrive. This filtered estimate helps distinguish persistent trends from quarterly noise in the observed house price series.

Out-of-sample backtest over 12 evaluation windows using the Dynamic Factor Model (DFM). Out-of-sample backtest over 12 evaluation windows using the Dynamic Factor Model (DFM). RMSE measures the typical forecast error in the same units as the series; 'naive' is a no-change benchmark. House Price Nowcast (RMSE 1.32 vs 0.66 naive, n=12).

Updated: 2026-06-06 by María López

Key Takeaways

Brent oil prices just jumped to $106.30 as of May 2026, reflecting a staggering YoY increase of 65.8%. Brent oil prices through May 2026 show a notable rise, landing at $106.30. This marks a significant YoY change of +65.8%, and the momentum is clearly up, with prices climbing in recent days. For Mexico, where oil is a major export and accounts for about 15% of federal revenue, these figures are crucial — they could bolster government finances and Pemex operations.

Copper prices are hitting $13,483.75, up 41.5% YoY as of May 2026. With copper data updated to May 2026, the current price stands at $13,483.75, showcasing a robust YoY increase of 41.5%. The trend remains upward, indicating strong demand in the global market. Given that Sonora dominates copper production in Mexico, this surge could enhance regional economic activity, despite the sector's small employment footprint.

Corn prices are at $215.62, reflecting a modest YoY increase of 5.3%. As of May 2026, corn prices reached $215.62, showing a slight YoY rise of 5.3%. The trend appears stable, neither soaring nor plummeting significantly. This is particularly relevant for Mexico, where corn is a staple for many, and price stability is key for the 1.5 million smallholder farmers dependent on this crop.

Commodity prices feed directly into Mexico's inflation pulse and terms of trade. Oil and corn affect energy and food costs, while copper is a proxy for global industrial demand. For policymakers, sharp commodity swings can shift inflation expectations and fiscal balances, making these prices critical to monitor.

Updated: 2026-08-08 by María López

Key Takeaways

The July 2026 IMSS release shows unit labor costs at -3.41%, indicating productivity is outpacing wage growth. Following July's formal sector wage data, ULC has dropped 1.18 percentage points from the previous month, signaling a concerning trend for labor conditions. This situation raises alarms about the sustainability of wage growth in the manufacturing sector, with real wages lagging behind productivity. If this gap persists, we could see increased tension in labor relations as workers demand fair compensation for their contributions.

Real wages in the formal sector reveal a mixed bag of outcomes for purchasing power. This divergence means while retail workers are experiencing growing financial confidence, those in manufacturing are facing shrinking budgets, which can lead to consumer spending slowdown. The widening gap could exacerbate economic inequality and social unrest if not addressed. It's imperative for policymakers to consider these dynamics as they plan future economic strategies.

Across sectors, the stark contrast in real wages emphasizes the uneven recovery from economic pressures. As manufacturing struggles, the retail sector's gains could signal a shift in consumer behavior and spending power. However, if manufacturing continues to lag, overall economic resilience may be jeopardized. Stakeholders must keep a close eye on these developments to ensure balanced growth across the economy.

SARIMAX Forecast Comparison

| Series | Current | Prev. Forecast | Error | 12M Forecast | Prev. 12M | Revision |

|---|---|---|---|---|---|---|

| ULC Manufacturing | — | — | — | -4.0 | -4.0 | +0.00 |

| ULC Retail | — | — | — | 1.5 | 1.5 | +0.00 |

| Real Wage Mfg | — | — | — | -2.4 | -2.4 | +0.00 |

| Real Wage Retail | — | — | — | 5.8 | 5.8 | +0.00 |

All values in % (MoM, seasonally adjusted). "Error" = actual − previous forecast. "Revision" = change in 12-month outlook. "—" = no prior forecast available.

Unit labor costs (ULC) measure the average cost of labor per unit of output — when wages grow faster than productivity, ULC rises, potentially squeezing profit margins and fueling inflation. In Mexico, where the formal sector employs roughly half the workforce, IMSS-registered wage data captures trends in the formal economy but misses the informal sector's dynamics. Real wages — nominal wages adjusted for inflation — determine household purchasing power and underpin consumer demand. For policymakers, these indicators help balance inflation control, competitiveness, and the economic welfare of Mexican workers.

Twelve-month-ahead forecasts for unit labor costs and real wages in manufacturing and retail are produced using a Seasonal Autoregressive Integrated Moving Average with eXogenous inputs (SARIMAX) model. The model is estimated on seasonally adjusted month-over-month percentage changes, with all four series — ULC manufacturing, ULC retail, real wage manufacturing, and real wage retail — entering as joint endogenous variables. No external auxiliary data feed the forecast; the model relies solely on the internal dynamics and cross-series interactions of the wage and productivity data. Forecast confidence intervals widen over the projection horizon.

Out-of-sample backtest over 24 evaluation windows using the SARIMAX. Out-of-sample backtest over 24 evaluation windows using the SARIMAX. RMSE measures the typical forecast error in the same units as the series; 'naive' is a no-change benchmark. ULC Manufacturing (RMSE 2.97 vs 3.21 naive, +7% improvement, n=24); ULC Retail (RMSE 5.33 vs 5.22 naive, n=23); Real Wage Manufacturing (RMSE 2.20 vs 2.62 naive, +16% improvement, n=24); Real Wage Retail (RMSE 3.05 vs 2.97 naive, n=23).

Updated: 2026-06-19 by Pablo Rivas

Key Takeaways

Following the recent updates in key economic indicators, real GDP growth in Mexico is now estimated at 4.96%, reflecting a robust upward revision of 2.66%. The latest quarterly GDP release from INEGI shows a marked increase in growth expectations, signaling a healthier economic outlook. This adjustment highlights a strong recovery trajectory, likely driven by resilient domestic consumption and improved industrial performance. As we advance into Q1 2026, this optimistic figure may bolster confidence among investors and policymakers alike.

Private consumption continues to be a key driver of growth. Household spending is estimated to have soared to 8.09%, significantly outpacing GDP growth. This robust expansion suggests that consumers are confident and willing to spend, providing essential support to overall economic activity. Such vigor in private consumption is a positive sign, signaling a thriving domestic market that can help buffer against external shocks.

Exports are struggling to keep up with domestic demand. External demand remains tepid, with export growth now at a mere 0.58%. This lackluster performance raises concerns about Mexico's competitiveness in the global market, especially as trading partners navigate their own economic uncertainties. The soft export figures could hint at challenges ahead for sectors reliant on international trade, potentially dampening the overall growth outlook.

Imports are indicating a shift in domestic absorption patterns. Imports have contracted to 1.56%, reflecting a 3.81% decline from previous estimates. This downturn signals a potential cooling in domestic demand, as consumers and businesses may be becoming more cautious in their spending habits. The drop in imports could also suggest that the economy is adjusting to current market conditions, though it may raise questions about future growth sustainability.

Net trade dynamics appear to be shifting. The trade balance contribution remains a mixed bag, as the decline in imports coupled with stagnant export growth presents a complex scenario. While fewer imports can ease some pressure on the trade deficit, the sluggish export performance raises flags about Mexico's economic resilience in a challenging global landscape. Policymakers will need to monitor these trends closely to ensure balanced and sustainable growth.

DFM GDP Nowcasts

| Component | Last Obs. (Q1 2026) | Nowcast (Q1 2026) | Prev. Nowcast | Revision |

|---|---|---|---|---|

| Real Gross Domestic Product | 6.19% | 4.96% | 4.96% | +0.00 |

| Private Consumption | 0.15% | 8.09% | 8.09% | +0.00 |

| Imports | 25.37% | 1.56% | 1.56% | +0.00 |

| Exports | 0.58% | 0.58% | 0.58% | +0.00 |

QoQ annualized, seasonally adjusted. Nowcast = DFM filtered estimate using higher-frequency inputs. "Revision" = change from previous run.

Real activity data tracks the economy's engine — output, spending, and trade — while nowcasts bridge the lag between releases. Real GDP captures total production; private consumption reflects household demand; exports and imports reveal external demand and the flow of inputs for Mexico's trade-exposed, manufacturing-heavy economy. Shifts in U.S. demand, global prices, and the peso often show up first in trade, then filter into GDP and consumption. Because official series arrive with delays and revisions, model-based nowcasts provide an early, probabilistic read for policy timing — useful if treated with uncertainty bands and cross-checked against higher-frequency signals.

A Dynamic Factor Model (DFM) nowcasts quarterly GDP and its demand components — private consumption, imports, and exports — using 14 higher-frequency inputs. These include monthly employment indicators, industrial production (IGAE), consumer confidence, capacity utilization, retail sales, and private consumption, plus quarterly GDP sector breakdowns. The model extracts common factors via the Kalman filter, updating the nowcast each time any input series receives new data. Nowcast estimates are conditional expectations that narrow as more data arrive within each quarter.

Out-of-sample backtest over 12 evaluation windows using the Dynamic Factor Model (DFM). Out-of-sample backtest over 12 evaluation windows using the Dynamic Factor Model (DFM). RMSE measures the typical forecast error in the same units as the series; 'naive' is a no-change benchmark. Real GDP (RMSE 3.90 vs 3.82 naive, n=12); Private Consumption (RMSE 5.41 vs 2.51 naive, n=12); Exports (RMSE 22.26 vs 18.28 naive, n=12); Imports (RMSE 11.34 vs 17.09 naive, +34% improvement, n=12).

Updated: 2026-07-25 by Pablo Rivas

Key Takeaways

The latest ENOE survey for May 2026 shows unemployment at 3.43%, reflecting a continued downward trend that has persisted for over four years. The May 2026 ENOE survey shows unemployment at 3.43%, around the 1st percentile historically and marking a decrease of 0.01% from April. This downward trajectory has been consistent, with the rate now on a 58-month streak of declines. The implications are clear: while the labor market appears to be tightening, ongoing structural challenges remain, particularly in relation to economic policy uncertainty.

By gender, male unemployment sits at 3.31%, while female unemployment is slightly higher at 3.48%. Male and female unemployment rates registered at 3.31% and 3.48%, respectively, indicating a modest divergence with women's unemployment slightly outpacing men's. Despite both rates trending downward, the persistence of this gap suggests different labor market dynamics at play, possibly influenced by sectoral employment differences and varying access to opportunities.

The share of informal workers in the economy has risen, now standing at 55.7%, which is concerning given its high percentile ranking. Informal employment has increased to 55.7%, reflecting a rise that points to economic insecurity as workers may be turning to less stable job arrangements. This trend signals potential weaknesses in the formal labor market, and a growing reliance on informal sectors could complicate efforts to improve overall economic stability.

DFM Employment Nowcasts

| Indicator | Last Obs. (Q2 2026) | Nowcast (Q2 2026) | Prev. Nowcast | Revision |

|---|---|---|---|---|

| Unemployment Rate | 2.75% | 3.43% | — | — |

| Underemployment Rate | 10.28% | 12.12% | — | — |

| Male Unemployment | 2.45% | 3.31% | — | — |

| Female Unemployment | 2.71% | 3.48% | — | — |

Observed = latest quarterly ENOE value. Nowcast = DFM filtered estimate using monthly auxiliary data. "Revision" = change from previous run.

Labor slack and its composition shape inflation pressure, policy timing, and social risk. Unemployment, underemployment, and unemployment by gender reveal how broad and uneven slack is. In Mexico's large informal sector, the informal employment share can swing sharply — often contracting faster in downturns as unprotected jobs are cut first, then rebounding early — masking true slack if headline unemployment alone is tracked. Tracking these dimensions helps distinguish cyclical slack from structural mismatches and calibrate monetary policy accordingly.

Between quarterly ENOE survey releases, a Dynamic Factor Model (DFM) nowcasts employment indicators using higher-frequency auxiliary data. The model ingests monthly series — industrial production, consumer confidence, capacity utilization, retail sales, and private consumption — alongside quarterly GDP components to extract common factors that track the business cycle. When any auxiliary series receives new data, the Kalman filter updates the nowcast, providing an early signal before the next official employment release.

Out-of-sample backtest over 20 evaluation windows using the Dynamic Factor Model (DFM). Out-of-sample backtest over 20 evaluation windows using the Dynamic Factor Model (DFM). RMSE measures the typical forecast error in the same units as the series; 'naive' is a no-change benchmark. Unemployment (RMSE 22.27 vs 0.13 naive, n=17); Underemployment (RMSE 1.26 vs 0.50 naive, n=11); Male Unemployment (RMSE 0.44 vs 0.26 naive, n=11); Female Unemployment (RMSE 0.44 vs 0.28 naive, n=11).

Updated: 2026-07-11 by María López

Key Takeaways

INEGI's Q2 2026 productivity release shows secondary sector output at 102, reflecting a slight decline of -0.79% from the previous month, but a modest increase of 0.313% from six months ago. Despite the recent dip, the aggregate index remains in the 81st percentile historically, suggesting robust underlying strength. This performance is largely driven by manufacturing, which continues to dominate the secondary sector with a hefty 66.57% share. While construction also holds up well at a healthy 85th percentile, mining is lagging significantly, underscoring a lack of broad-based growth across all subsectors.

Across the PCA indices, manufacturing composites show a concerning divergence between productivity and labor demand metrics. Productivity has slipped by -0.223%, while sales increased slightly by 0.0281%, indicating a potential buildup of inventory pressure. This misalignment raises sustainability concerns as firms may face challenges in maintaining output levels amid rising costs and declining demand for labor.

Within manufacturing, the top-performing subsectors include transport equipment and food, both showcasing resilience amid overall sector fluctuations. Transport equipment experienced a notable rise of 2.99%, while the food subsector remains strong at the 84th percentile. In contrast, the petroleum and coal products sector is struggling, with a significant decline of -10.5%, which reflects broader issues in energy pricing affecting manufacturing dynamics.

PCA Composite Indices

| Index | May 2025 | Jun 2025 | Δ |

|---|---|---|---|

| Productivity Index | 0.50 | 0.28 | -0.22 |

| Sales Index | 0.58 | 0.61 | +0.03 |

| Inventory Index | 0.15 | -0.03 | -0.18 |

| Labor Demand Index | -1.32 | -1.49 | -0.17 |

Standardized scores (0 = mean, ±1 = one standard deviation).

Productivity trends reveal the economy's capacity to grow without stoking inflation. In Mexico, productivity in the secondary sector — mining, energy, construction, and especially manufacturing — signals how efficiently output expands relative to inputs. Strong productivity gains mean firms can meet demand without raising prices, easing inflation pressure and supporting sustainable wage growth. Weak productivity, by contrast, constrains supply, making cost shocks more inflationary. Manufacturing deserves closer scrutiny, as its diverse subsectors respond differently to global demand, exchange rate shifts, and investment cycles. Tracking these patterns helps judge whether growth is supported by efficiency gains or reliant on credit and labor cost increases.

Four composite indices — productivity, sales, inventory, and labor demand — are constructed using Principal Component Analysis (PCA) applied to INEGI manufacturing subsector data and GDP sector composition. PCA extracts the dominant co-movement pattern across subsectors, producing standardized indices that summarize broad trends while filtering out subsector-specific noise. The productivity index draws on output-per-worker measures across manufacturing branches; the sales, inventory, and labor demand indices use INEGI's corresponding survey-based indicators supplemented by GDP sector weights.

Updated: 2026-08-04 by Ignacio Crane

INEGI's latest July 2026 release reveals confidence at an elevated level, with the general index standing at 1.35, placing it in the 90th percentile. The July 2026 consumer confidence survey shows the general index at 1.35, reflecting a notable improvement in sentiment, particularly against a backdrop of ongoing economic uncertainty. This increase of 0.22 signals a robust consumer outlook, heightened by the recent upward trend in general confidence. However, a stark divergence is evident in the housing-specific index, which remains relatively subdued at 0.29, suggesting that while overall sentiment is optimistic, the housing sector continues to lag behind, potentially due to lingering concerns over affordability and market stability.

PCA Confidence Indices

| Index | Jun 2026 | Jul 2026 | Δ |

|---|---|---|---|

| General Sentiment | 1.14 | 1.35 | +0.22 |

| Housing Appetite | 0.07 | 0.29 | +0.21 |

| Durables Appetite | 1.70 | 1.73 | +0.03 |

Values are z-scores (0 = historical mean, ±1 = one standard deviation).

The ENCO (Encuesta Nacional sobre Confianza del Consumidor) is conducted jointly by INEGI and Banco de México. Roughly 2,300 households across 32 major cities are interviewed during the first 20 days of each reference month, and results are published around the 5th of the following month. The survey uses a rotating panel design — each household stays in sample for four consecutive months, rests for eight, then returns for four more — which smooths out idiosyncratic response noise while capturing genuine shifts in sentiment. Because confidence data arrive before most hard activity indicators for the same month, they provide an early read on whether household demand is strengthening or cooling.

Three composite confidence indices — general sentiment, housing appetite, and durables appetite — are extracted from the eight raw INEGI survey questions using Principal Component Analysis (PCA). PCA identifies the common variation within each question group, producing a single index that captures the dominant signal while filtering out question-specific noise. The general index draws on six broad economic outlook questions; the housing and durables indices each isolate spending appetite in categories most sensitive to interest rates and household balance sheets.

Updated: 2026-08-01 by Ignacio Crane

Key Takeaways

News-based policy uncertainty in July 2026 stands at 18.34% of articles tagged policy-uncertain. Mexican news coverage of policy uncertainty reveals a significant level, with 18.34% of articles reflecting this theme, marking a decline from the previous three-month average of 20.0%. Over the past year, however, this metric has risen by 2.9%, indicating a persistent elevation in concerns surrounding economic policy. The most recent month shows a modest decline of 1.7%, suggesting a slight easing in the immediate perception of uncertainty.

By category, the latest data indicates that trade policy is the most significant driver of recent uncertainty. Within the uncertainty narrative, trade policy has emerged as the single largest mover over the last three months, increasing by 2.1 percentage points to 9.43%. Additionally, the labor market and regulation categories have also contributed to the composition of uncertainty coverage, albeit to a lesser extent. This highlights a growing concern among stakeholders regarding the implications of trade dynamics on economic stability.

Compared with the officially published BBD index, the news-derived measure shows a similar downward trajectory. Against the Baker-Bloom-Davis benchmark, which reported a reading of 149.8 for June 2026, both indices reflect a notable decline in policy uncertainty over the past three months. The alignment of these measures reinforces the narrative that while concerns persist, there is a trend towards reduced uncertainty in the short term. This convergence may provide policymakers with a more favorable context for decision-making in the coming months.

The Economic Policy Uncertainty (EPU) index tracks the share of Mexican news articles whose text matches terms spanning three categories — the economy, uncertainty, and policy — scraped daily from five major outlets since 2015 and aggregated into daily, weekly, and monthly indices across 15 policy categories (monetary, fiscal, trade, regulation, and more). This news-derived measure is compared against the externally-published Baker-Bloom-Davis (BBD) Mexico EPU index (policyuncertainty.com), the original academic methodology on which this approach is based. Because uncertainty coverage often front-runs formal policy announcements, the index provides an early, text-based signal of shifting attention toward economic policy risk.

Updated: 2026-08-04 by Ignacio Crane

Key Takeaways

The July 2026 SPF survey shows the aggregate Concern Index at 2.79, positioned around the 60th percentile. The July 2026 SPF survey shows the aggregate Concern Index at 2.79, positioned around the 60th percentile. This reflects a modest decline of -0.04 compared to the previous month. The sustained downward trend over the past three months indicates a potential easing in economic anxiety, although the index remains higher compared to the same period last year, suggesting lingering concerns within the economic landscape.

Economists have identified public insecurity, US trade policy, and the lack of structural change as the most pressing growth constraints currently cited. The key constraints currently cited include public insecurity at 10.39%, US trade policy at 7.62%, and a lack of structural change at 4.39%. Notably, public insecurity is the single biggest month-over-month mover, having increased by 1.20%. This uptick underscores a persistent challenge that could impact overall economic stability and growth prospects.

The perceived probability of recession among surveyed economists stands at 25.0%, indicating moderate concerns relative to historical norms. The perceived probability of recession currently reflects moderate unease, with a probability of 25.0%, which is positioned at the 76th percentile historically. This suggests a heightened awareness of potential economic downturns compared to previous quarters. Looking ahead, expectations for the next quarter show a slight decline in recession probability to 20.2%, indicating a cautiously optimistic outlook among forecasters.

According to forecasters, the FX forecast misalignment indicates that the peso is perceived as overvalued across multiple horizons. FX expectations suggest that forecasters see the peso as overvalued, with a current misalignment of +0.039. This perspective persists across the one- and two-month outlooks, signaling a consistent sentiment regarding the peso's strength. Such assessments may influence monetary policy considerations, particularly in relation to inflation dynamics and currency stability.

Banxico's Survey of Professional Forecasters (Encuesta sobre las Expectativas de los Especialistas en Economía del Sector Privado) polls roughly 40 groups of analysts from banks, financial institutions, consultancies, and research centers. Responses are collected during the second half of each reference month — typically between the 15th and 28th — and results are published on the first business day of the following month. Because respondents form their expectations before some end-of-month official data releases, the survey provides an early window into shifting professional sentiment on inflation, growth constraints, recession risk, and exchange rates, making it a valuable leading indicator for policymakers and market participants.

Updated: 2026-08-11 by Ignacio Crane

As of 2026-08-11, bond prices reveal an intriguing landscape in the yield curve, with the nominal 10Y-3Y spread standing at 1.32%, reflecting a modest increase of 0.10% from the previous observation. The latest yield curve data reveals that the nominal spread is currently normal, following a streak of three days of decline, while the real spread maintains its normal status, reflecting evolving expectations amidst global economic pressures. The breakeven inflation spread's increase implies that investors are factoring in potential inflation risks, albeit within a controlled framework. As markets continue to navigate uncertainty, these spreads serve as critical indicators of sentiment and expectations.

The curve shape suggests a potential dovish tilt in monetary policy, with markets pricing in a 20 basis point cut by Banxico, driven by declining headline inflation and rising economic policy uncertainty. Markets appear to be pricing in a more aggressive easing cycle than what may be warranted by the current economic landscape, reflecting a disconnect between market sentiment and the prevailing policy consensus. Given the emphasis on data-driven decisions articulated by Banxico, the trajectory of the yield curve will be closely monitored for signs of alignment or further divergence in the weeks to come.

Yield Spread Update

| Spread (10Y−3Y) | 07 Aug | 10 Aug 2026 | Δ | NS-DFM |

|---|---|---|---|---|

| Nominal | 1.33 | 1.32 | -0.008 | 0.62 |

| Real | 0.61 | 0.56 | -0.053 | 0.28 |

| Inflation | 0.72 | 0.77 | +0.045 | 0.35 |

All values in percentage points. NS-DFM = Nelson-Siegel Dynamic Factor Model filtered estimate.

When investors and businesses trust that monetary policy will remain credible and predictable, long-term interest rates respond more smoothly to central bank signals. Yield curve spreads between long and short maturities serve as a real-time gauge of this alignment: a stable, upward-sloping curve suggests markets expect gradual normalization, while persistent inversions often signal that markets anticipate policy shifts before they are announced. For Mexico, where inflation targeting depends on anchoring expectations across a diverse investor base, the 10-year minus 3-year spread offers a compact summary of whether policy communication is landing as intended.

Yield curve spreads are filtered using a Nelson-Siegel Dynamic Factor Model (NS-DFM) estimated on weekly data. The model ingests 16 synthetic yield curve points — 11 nominal maturities (overnight through 30 years) and 5 real maturities (overnight through 30 years) — fitted via Nelder-Mead optimization on Banxico bond prices. Factor loadings follow the Diebold-Li (2006) Nelson-Siegel parameterization, decomposing each yield curve into level, slope, and curvature components for both real rates and implied inflation. The Kalman smoother extracts filtered spread estimates that track the underlying signal in daily bond market noise.

Updated: 2026-08-11 by Ignacio Crane

Key Takeaways

Mexican equity markets as of August 11, 2026, show excess returns at 0.0283, reflecting a modest upward trend amidst ongoing economic uncertainties. With data through August 11, 2026, realized volatility stands at 0.0093, indicating a slight decline in market responsiveness. Notable revisions in volatility metrics, including a downward adjustment in risk-return to -0.15 and an increase in illiquidity as measured by Amihud to 80.62, suggest a tightening market environment. These dynamics may imply a cautious approach from investors as they navigate the complexities of the current economic landscape.

The decomposition shows that recent volatility has been driven primarily by US policy shocks and real-sector difficulties. Top contributors to the recent volatility shifts include heightened investor sentiment and ongoing liquidity concerns, underscoring persistent external pressures. The interplay of these factors has led to a nuanced market reaction, reflecting the uncertainty surrounding both domestic and international economic conditions.

Investor sentiment remains tepid, with indicators suggesting a rising level of economic policy uncertainty. Current levels of sentiment, as illustrated by the American Association of Individual Investors (AAII) and the National Association of Active Investment Managers (NAAIM), reflect apprehension in the face of escalating domestic security issues and external economic pressures. This environment of uncertainty is likely to influence decision-making among fund managers and corporate treasurers alike, as they weigh the potential for future volatility against the backdrop of a fragile economic recovery.

Volatility Measures

| Measure | Jul 2026 | Aug 2026 | Δ | Top Driver |

|---|---|---|---|---|

| Excess Return | -0.0269 | -0.1495 | -0.1226 | Real-Sector Difficulties (+0.058) |

| Realized Volatility | 0.0083 | 0.0073 | -0.0010 | Uncertainty (-0.001) |

| Illiquidity (Amihud) | 99.8026 | 80.6197 | -19.1829 | Uncertainty (-13.192) |

Monthly averages. Top Driver = largest OLS category contribution to latest value.

Financial market returns, volatility, and liquidity signal investor sentiment and risk appetite. Excess returns over government bonds capture the risk premium investors demand for holding equities; wider spreads suggest higher perceived risk or stronger growth prospects. Realized volatility in a stock market index reflects uncertainty — sharp swings indicate fragile sentiment and raise the cost of capital. Illiquidity shows how trading volume and price impact interact: when liquidity dries up, small trades can move prices disproportionately, amplifying shocks. For monetary policy, these indicators matter because they shape funding costs, investment flows, and the broader transmission of rate decisions into financial conditions.

Volatility drivers are analyzed in two steps. First, Principal Component Analysis (PCA) groups the six SPF concern categories and investor sentiment indicators (AAII bull-bear spread, NAAIM exposure index) into thematic driver clusters that capture common variation. Second, an OLS regression decomposes recent volatility movements into contributions from each driver cluster, quantifying how much of the observed excess return and realized volatility is attributable to policy uncertainty, external sentiment, and domestic macro conditions. The decomposition is descriptive — it identifies contemporaneous associations, not causal effects.

Updated: 2026-08-11 by Ignacio Crane

Key Takeaways

Banxico's August 2026 credit release shows money market spreads tightening, indicating a cautious lending environment as economic pressures mount. Following the latest August lending data, rate premia stand at 0.168, reflecting a narrowing trend in funding spreads relative to the policy rate. This represents a significant tightening of -0.0817 since the previous month and a continued contraction over the past year. The narrowing spread suggests an increasing reluctance among financial institutions to extend credit, possibly due to heightened economic uncertainty and the evolving monetary policy landscape.

Household mortgage rates remain elevated, presenting affordability challenges for potential homebuyers. The total annual cost of mortgages averages 13.8%, with a range from 10.7% to 28.2%. This persistent high cost underscores the limited pass-through of recent policy rate adjustments, which may hinder borrowing capacity and weigh on the housing market as consumers face increasing financial pressures.

Debt issuance patterns show a notable preference for fixed-rate financing, reflecting a shift in corporate risk management strategies. Currently, fixed-rate debt accounts for 19.47% of GDP, while variable (inflation-linked) and other variable rates comprise 10.11% and 9.71%, respectively. This composition indicates firms are leaning towards stability in their financing amid rising interest rate expectations, although the overall debt issuance remains at a historical low, signaling potential caution in corporate investment strategies.

Rate premia show how market and bank funding costs move relative to the policy rate, indicating the efficiency of monetary transmission. Household mortgage rates capture the cost of long-term borrowing — their sharp rise in recent years signals affordability pressures and distributional effects, as many families face double-digit costs. Debt issuance patterns, normalized by GDP, reveal how firms finance themselves; the balance between fixed and variable rates matters for vulnerability to policy shifts. Together, these indicators show how policy rates filter into real borrowing conditions, affecting credit demand, investment, and ultimately growth and inflation dynamics.